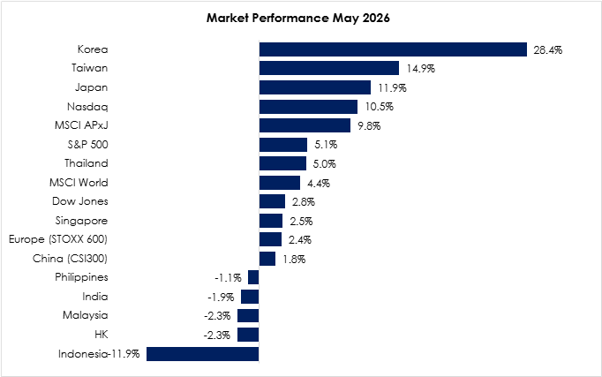

The MSCI Asia Pacific Ex-Japan Index (+9.8%) once again outperformed the MSCI World Index (+4.4%) as tech supply chain beneficiaries continued to dominate headlines and hyperscaler capex spend. South Korea’s (+28.4%) KOSPI went on a tear, already doubling in value year-to-date as memory executives foresee chip shortages lasting until 2030. Taiwan (+14.9%) followed suit, with TSMC reportedly having Nvidia become its top customer, beating Apple. Thailand (+5.0%) had recovered to 3-year highs despite a declining tourism scene and weaker private consumption. Indonesia (-11.9%) fell to 5-year lows as MSCI cut 6 companies from its Indonesia index, signalling the persistent governance and transparency issues plaguing the country. Hong Kong (-2.3%) dropped despite strong retail sales data on stronger tourism and resilient consumption sentiment. Malaysia (-2.3%) also declined on weaker outlook and guidance for banking and consumer-related stocks.

Exhibit 1: Market Performance May 2026

Source: Bloomberg, PCM, 31 May 2026

The MSCI World Index gained (+4.4%) during the month, driven by strong performance in technology and AI-related stocks, easing trade policy uncertainties, and improving investor confidence in the global growth outlook. Within Developed Markets, Japan (+11.9%) led market gains, supported by strong foreign investor inflows, continued progress in corporate governance reforms, and robust performance of AI-related semiconductor companies. These positive factors helped offset concerns over a weaker yen, geopolitical tensions, and broader macroeconomic uncertainties, reinforcing investor confidence in the Japanese equity market. The US also rallied (+5.1%), supported by a recovery in large-cap technology stocks and continued optimism surrounding AI-driven earnings growth. Europe (+2.4%) posted solid returns, supported by improving economic momentum, resilient corporate earnings, and growing expectations of policy easing by the European Central Bank, while sentiment was also aided by easing concerns over energy supply disruptions, although geopolitical tensions and uneven regional growth continued to weigh on investor conviction.

On the monetary policy front, the Reserve Bank of Australia (RBA) set its official cash rate at 4.35% following a 25 basis points hike in May 2026, as policymakers assessed persistent inflation and resilient domestic demand. Within ASEAN, Bank Indonesia raised its benchmark interest rate by 50 bps to 5.25% at its May 2026 policy meeting, in a move aimed at supporting rupiah stability amid external pressures, anchoring inflation expectations, and maintaining financial market stability in the face of tighter global monetary conditions, while Bank Negara Malaysia maintained its Overnight Policy Rate at 2.75% in May 2026, as it continued to balance growth support with price stability.

The FBMKLCI Index declined by 2.3% month-on-month (m-o-m) in May, closing at 1,683.07 points. Meanwhile, the FBM Hijrah Shariah Index fell by 2.0% in May, the Mid 70 Index gained by 2.2%, while the Small Cap Index declined by 1.0%. Sector-wise in May, the top-performing sectors were Technology, Utilities, and Healthcare, which rose by 19.0%, 2.8%, and 2.2% m-o-m, respectively. The worst-performing sectors were Energy, Consumer, and Plantation, which declined by 7.4%, 5.9%, and 4.9% m-o-m, respectively.

Within the KLCI, the top three gainers for May were YTL Power International Bhd (+6.7%), Maxis Bhd (+6.0%), and Press Metal Aluminium Holdings Bhd (+4.2%). Meanwhile, the top three decliners were Petronas Dagangan Bhd (-12.6%), Nestle Malaysia Bhd (-11.6%), and Axiata Group Bhd (-11.1%).

Foreign investors were net seller, with a net outflow of RM3.6 billion, bringing the year-to-date (YTD) outflows to RM1.9 billion. Separately, in May, there was one listing on the Main Market (Skyechip Bhd), four listings on the ACE Market (Manforce Group Bhd, Inspace Creation Bhd, Gold Li Holdings Bhd, Ei Power Bhd), and two listings on the LEAP Market (Milolo Bhd, Noesis Exed Bhd)

For the month of May, WTI crude oil declined by 16.9% m-o-m to US$87.4 per barrel, while Brent crude fell by 19.3% m-o-m to US$92.1 per barrel. Crude palm oil declined to RM4,470/MT, down 0.8% from the previous month, while spot gold declined by 1.5% to US$4,560/oz. Currency-wise, the Malaysian ringgit appreciated by 0.2% m-o-m against the greenback to RM3.9645/USD. Meanwhile, the Dollar Index rose by 0.9% to 99.0 points.

Equity Market Outlook & Investment Strategy

Malaysia

Malaysia is expected to maintain a gradually stabilising, though still cautious, macro backdrop in June as global volatility continues to moderate. However, external demand remains uneven, with mixed growth signals from the US and China continuing to affect export momentum and the ringgit. Domestic demand remains the key support, underpinned by resilient household spending and stable labour market conditions. Against this backdrop, we stay constructive on selected domestic-oriented sectors, especially those linked to rising electricity demand from data centre expansion and continued momentum in renewable energy investment. We are also increasingly positive on the technology sector as visibility in order flows improves, supported by sustained AI-related capex from global leaders. Accordingly, our strategy continues to favour a barbell approach anchored on large-cap, high-quality companies with strong balance sheets and reliable dividend yields, while selectively complemented by exposure to firms with clear earnings growth potential from structural thematic drivers.

Regional

Recent developments in the Middle East, including reported progress in maintaining a conditional ceasefire between Iran and the United States, have helped ease some geopolitical tensions and support a more stable risk backdrop into mid-2026. This gradual improvement in global risk sentiment is constructive for broader markets, particularly for manufacturing and semiconductor equipment sectors, which continue to be underpinned by strong structural demand from AI infrastructure, data centre expansion, renewable energy deployment, and advanced memory technologies such as DRAM and HBM.

While near-term volatility arising from Middle East-related supply chain risks may persist, we view such episodes as opportunities for disciplined long-term positioning. Although sector leadership continues to be driven by AI infrastructure and its global supply chain beneficiaries, the market is becoming increasingly selective as valuations turn more demanding.

In this environment, we believe a barbell strategy that combines growth and income exposures, alongside broader diversification, remains well positioned to navigate volatility stemming from potential energy shocks, renewed inflationary pressures, and lingering uncertainties surrounding US tariff policies.

Fixed Income Outlook & Strategy

Malaysia

Malaysia’s bond market outlook remains constructive, supported by resilient growth, contained inflation, and steady foreign inflows. GDP growth of 5.4% in 1Q2026 reflects sustained domestic demand, while inflation at 1.9% remains manageable despite upside risks from elevated energy prices. Bank Negara Malaysia is expected to keep the OPR at 2.75%, maintaining a cautious but stable policy stance. Going forward, rates are likely to stay range-bound, with direction driven mainly by external factors such as US Treasury movements, global risk sentiment, and oil price volatility.

Regional

US Treasury yields were highly volatile in May 2026, driven by developments in the US–Iran conflict, sharp fluctuations in oil prices, and shifting inflation expectations. Escalating tensions and the prolonged disruption of shipping through the Strait of Hormuz pushed crude oil prices above USD100 per barrel, fuelling concerns over energy-driven inflation and causing a bear flattening of the yield curve, with the 30-year Treasury yield briefly rising above 5.0%. However, subsequent signs of progress in diplomatic negotiations triggered a decline in oil prices and supported a rally in Treasuries as inflation concerns eased. Economic data remained broadly resilient, with April nonfarm payrolls rising by 115,000, the unemployment rate holding at 4.3%, and jobless claims remaining relatively low, indicating continued labour market strength. Against this backdrop, Federal Reserve officials maintained a cautious stance, highlighting persistent inflation risks while signalling limited urgency to ease policy, reinforcing market expectations that interest rates would remain unchanged for an extended period.

Japan Prime Minister Sanae Takaichi announced a supplementary budget of JPY3trn (USD19bn) to subsidise fuel costs and ease cost-of-living pressures amid surging energy prices fuelled by the ongoing Iran war and rising import costs from the weak yen.

The People’s Bank of China (PBoC) maintained its key lending rates at record lows for a 12th consecutive month in May 2026, with the 1-year Loan Prime Rate held at 3.0% and the 5-year LPR at 3.5%, reflecting a continued moderately accommodative policy stance aimed at stabilising growth amid external and domestic uncertainties. This policy decision came alongside mixed but improving activity signals, as the RatingDog China General Manufacturing PMI rose to 52.2 in April from 50.8, marking the fastest expansion since December 2020. The improvement was driven by stronger new orders and accelerating output growth, although supply chain pressures intensified due to higher input costs, logistics disruptions, and elevated energy prices linked to Middle East tensions. At the same time, inflationary pressures picked up, with both input and output prices rising to multi-year highs, highlighting an emerging policy balancing act between supporting growth and managing cost-driven inflation risks.

Strategy for the month

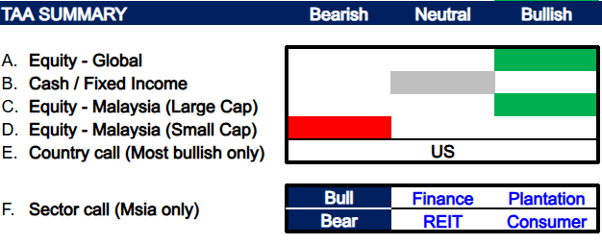

We continue to favor global equities, particularly the U.S., supported by the resilience of the U.S. economy, strong domestic consumption, and its position as a major energy producer and net exporter. Recent de-escalation in U.S.–Iran tensions has also helped improve global risk sentiment and eased concerns over a prolonged energy shock. More importantly, the U.S. market remains home to world-leading companies with strong earnings visibility, particularly in the technology sector. While valuations are stretched, they are supported by robust earnings growth, rising AI-related capital expenditure from hyperscalers, and continued strong results and guidance from leading AI beneficiaries across semiconductors, cloud computing, and digital infrastructure reinforcing the structural growth outlook for the sector.

In Malaysia, we adopt a bullish view on large-cap equities and remain bearish on small-cap equities. Sector-wise, we overweight Finance and Plantation, supported by resilient domestic fundamentals, healthy credit expansion and stable asset quality, which should sustain banking sector earnings and shareholder returns. Plantation is expected to remain supported by firm CPO prices, driven by structural biodiesel demand, tight global vegetable oil supplies and potential weather-related production risks, providing continued earnings support for the sector. Meanwhile, we are bearish on REITs (potential pressure from higher interest rates amid lingering inflation concerns), and Consumer sector (pressure from elevated input costs driven by global energy prices and ongoing supply chain disruptions).

Exhibit 2: PCM’s monthly strategy snapshot

Source: PCM, 31 May 2026

Phillip Capital Malaysia and our offerings

We reaffirm our belief that there are still opportunities in the market, and we maintain a discerning approach in choosing high-quality stocks for our portfolio. However, it is crucial to exercise caution and carefully select investment options to ensure the best risk-adjusted returns. By taking a vigilant and discerning approach, investors can potentially reap the benefits of the current market opportunities while minimising risks.

A noteworthy avenue for investors seeking diversification in their portfolio is through PhillipCapital Malaysia. PhillipCapital Malaysia offers multiple private mandate services managed by professional fund managers. By leveraging PhillipCapital Malaysia’s private mandate services, investors can enhance their resiliency, optimise portfolio performance, and navigate the complexities of the market with confidence.

We also offer both conventional and Shariah-compliant options to cater to the needs of all investors. For Malaysia’s mandates, we like:

1. PMART/PMA Dividend Enhanced and/or PMART/PMA Dividend Enhanced ESG

Our PMART Dividend Enhanced and PMA Dividend Enhanced is an income-driven portfolio focused on high dividend-yielding equities. We apply the Dog of the Dow approach, screen and select top market cap stocks to minimise risk and ensure consistent performance. The portfolio is an equal weighting portfolio which reduces concentration risk and provides similar exposure to all clients, both initially and after rebalancing. We offer both conventional and Shariah investment options to cater to the diverse needs of our investors. Click here to learn more. We recently also introduced PMART/PMA Dividend Enhanced ESG Mandate as we remain dedicated to investing in ESG stocks given their stronger valuation and profitability.

2. PMART/PMA ESG

Phillip Capital Malaysia offers discretionary portfolio that invests in stocks with high ESG ratings from the F4GBM and F4GBMS Indices, namely PMART and PMA ESG. There are both conventional and Shariah options available. To explore the companies in which both Conventional and Shariah ESG mandates invest, you can refer to the provided link.

3. PMART/PMA Blue Chip and Opportunity

Our Blue-Chip portfolios primarily allocate our investments towards companies with large market capitalisations, while the Opportunity portfolios predominantly invest in companies with smaller market capitalisations. We also offer both conventional and Shariah-compliant options to cater to the needs of all investors.

Please click on the link to learn more or email us at cse.my@phillipcapital.com.my if you require any further information.

Disclaimer

The information contained herein does not constitute an offer, invitation, or solicitation to invest in any product or service offered by Phillip Capital Management Sdn Bhd (“PCM”). No part of this document may be reproduced or circulated without prior written consent from PCM. This is not a unit trust or collective investment scheme and is not an obligation of, deposit in, or guaranteed by PCM. All investments carry risks, including the potential loss of principal.

Performance figures presented may reflect model portfolios and may differ from actual client accounts’ performance. Variations in individual clients’ portfolios against model portfolios and between one client’s portfolio to another can arise due to multiple factors, including (but not limited to) higher relative brokerage costs for smaller portfolios, timing of capital injections or withdrawals, timing of purchases and sales, and mandate change (e.g., Shariah vs. conventional). These differences may impact overall performance.

Past performance is not necessarily indicative of future returns. The value of investments may rise or fall, and returns are not guaranteed. PCM has not considered your investment objectives, financial situation, or particular needs. You are advised to consult a licensed financial adviser before making any investment decisions.

While all reasonable care has been taken to ensure the accuracy and completeness of the information contained herein, no representation or warranty is made, and no liability is accepted for any loss arising directly or indirectly from reliance on this material. This publication has not been reviewed by the Securities Commission Malaysia.

{kind=link}