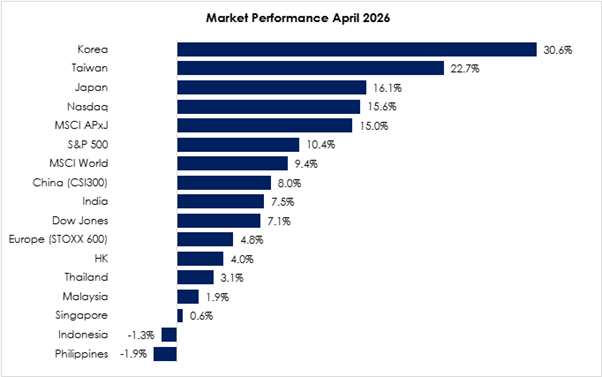

The MSCI Asia Pacific Ex-Japan Index (+15.0%) charted its highest monthly gain in 3 years, considerably outclassing the MSCI World Index (+9.4%) as regions with advanced chips exposure staged strong double-digit returns in April. South Korea (+30.6%) completely retraced its March losses and continued to record all-time highs, with leading index names such Samsung Electronics and SK Hynix are forecasted by institutional sell-side research to be the top 2 world’s most profitable companies by 2027. Taiwan (+22.7%) shared in the comeback rally as not only TSMC charted all-time highs but data centre infrastructure and ASIC names also surged tremendously on value chain-wide optimism. China (+8.0%) trailed the 2 exceptional leaders and bucked expectations as its market rallied markedly in defiance of the Strait of Hormuz closure impeding its energy supply. Philippines (-1.9%) sold off to the bottom of its 6-year trading range, indicating weak sentiment for the economy as a whole amidst energy concerns and a weakening peso. Indonesia (-1.3%) continued its decline for the 4th month in a row, pressured by ongoing concerns from the earlier MSCI transparency issues and elevated oil prices.

Exhibit 1: Market Performance April 2026

Source: Bloomberg, PCM, 30 April 2026

The MSCI World Index gained (+9.4%) during the month, reflecting a strong rebound in global equities amid improving risk sentiment and resilient earnings expectations. Within Developed Markets, Japan (+16.1%) led the advance, benefiting from continued investor inflows and solid corporate performance, despite lingering concerns of energy prices and geopolitical risks. The US also rallied (+10.4%), supported by a recovery in large-cap technology stocks and optimism around AI-driven earnings growth. Finally, Europe (+4.8%) posted solid returns, supported by improving economic momentum and easing investor concerns around energy shocks, even as geopolitical tensions remained a key overhang.

On the monetary policy front, the Federal Reserve kept the federal funds rate unchanged within the 3.50%–3.75% target range at its April 2026 meeting. The European Central Bank (ECB) also left its deposit rate unchanged at 2.00% at its April meeting. Meanwhile, the Bank of Japan maintained its key short-term policy rate at 0.75%. Meanwhile, core PCE inflation, the Federal Reserve’s preferred measure, rose to 3.2% yoy in March, compared to 3.0% in February. At the same time, the US unemployment rate eased to 4.3% in March, from 4.4% in February.

The FBMKLCI Index gained by 1.9% month-on-month (m-o-m) in April, closing at 1,722.02 points. Meanwhile, the FBM Hijrah Shariah Index gained by 4.4% in April, the Mid 70 Index gained by 7.2%, while the Small Cap Index gained by 6.6%. Sector-wise in April, the top-performing sectors were Technology, Construction, and Property, which rose by 22.9%, 11.6%, and 10.4% m-o-m, respectively. The worst-performing sectors were Finance and Plantation, which declined by 0.7%, and 0.5% m-o-m, respectively.

Within the KLCI, the top three gainers for April were YTL Power International Bhd (+31.7%), YTL Corp Bhd (+26.7%), and Gamuda Bhd (+17.9%). Meanwhile, the top three decliners were Sunway Healthcare Holdings Bhd (-9.6%), Petronas Dagangan Bhd (-8.9%), and AMMB Holdings Bhd (-6.4%).

Foreign investors were net buyer, with a net inflow of RM450.3 million, bringing the year-to-date (YTD) inflows to RM3.2 billion. Separately, in April, there were two listings on the Main Market (Empire Premium Food Bhd, MTT Shipping and Logistics Bhd) and three listings on the ACE Market (5E Resources Holdings Bhd, Golden Destinations Group Bhd, AMS Advanced Material Bhd).

For the month of April, WTI crude oil rose by 3.6% m-o-m to US$105.1 per barrel, while Brent crude declined by 3.7% m-o-m to US$114.0 per barrel. Crude palm oil declined to RM4,504/MT, down 4.8% from the previous month, while spot gold declined by 0.4% to US$4,629/oz. Currency-wise, the Malaysian ringgit appreciated by 2.0% m-o-m against the greenback to RM3.9717/USD. Meanwhile, the Dollar Index declined by 2.0% to 98.1 points.

Equity Market Outlook & Investment Strategy

Malaysia

Malaysia is expected to see a gradually stabilising, though still cautious, macro environment in May as global volatility eases. However, external demand uncertainty, driven by uneven growth in the US and China, continues to weigh on export visibility and the ringgit. Domestic demand remains the key growth anchor, supported by resilient consumer spending and steady labour market conditions. Against this backdrop, we are constructive on selected domestic-oriented sectors, particularly those benefiting from accelerating power demand from data centres and the ongoing push for renewable energy development. We are also turning more positive on the technology sector as order visibility improves, supported by continued strong capex guidance from global AI leaders. Accordingly, our strategy continues to emphasize a barbell approach — focusing on large-cap quality companies with defensible moats and sustainable dividend profiles, while selectively balancing exposure with companies offering strong and visible earnings growth from sectors benefiting from the current thematic trends highlighted above.

Regional

Following recent efforts to de-escalate tensions, Iran and the United States have reportedly agreed to extend a conditional ceasefire, signalling further progress toward reducing geopolitical risks in the region. The gradual improvement in geopolitical conditions reinforces a more constructive market outlook for the remainder of 2026, particularly for the global manufacturing and semiconductor equipment sectors, which continue to benefit from robust demand linked to AI infrastructure, data centres, renewable energy development, and advanced memory technologies such as DRAM and HBM.

While near-term volatility arising from Middle East-related supply chain risks may persist, we view such episodes as opportunities for disciplined long-term positioning. Although sector leadership continues to be driven by AI infrastructure and its global supply chain beneficiaries, the market is becoming increasingly selective as valuations turn more demanding.

In this environment, we believe a barbell strategy that combines growth and income exposures, alongside broader diversification, remains well positioned to navigate volatility stemming from potential energy shocks, renewed inflationary pressures, and lingering uncertainties surrounding US tariff policies.

Fixed Income Outlook & Strategy

Malaysia

Looking ahead, on the domestic front, Bank Negara Malaysia is expected to maintain the Overnight Policy Rate (OPR) at 2.75% in the near term, reflecting a still-balanced growth-inflation trade-off. Malaysia’s resilient growth trajectory of 4–5% and manageable inflation profile 2% support policy stability, although upside inflation risks from global energy prices warrant continued vigilance. As such, BNM is likely to adopt a wait-and-see approach through 2026, with any policy adjustment contingent on clearer evidence of sustained inflationary pressures or a material shift in growth dynamics.

Regional

U.S. Treasury (UST) yields exhibited pronounced volatility in April but ultimately shifted higher, with the 10-year benchmark gravitating toward the 4.40% range, extending the upward repricing observed since late 1Q. Early-month declines, supported by a temporary easing in geopolitical tensions, softer macroeconomic data, and a shift toward expectations of policy easing, were later reversed as inflation concerns resurfaced, driven largely by renewed strength in energy prices. The April FOMC meeting delivered a hawkish hold, maintaining the policy rate at 3.50%–3.75%, while signalling heightened concern over inflation persistence and reducing forward guidance toward near-term easing. This recalibration, alongside elevated term premia and ongoing Treasury supply pressures, drove a bear-steepening bias at various points in the month.

Looking ahead, UST yields are expected to remain upwardly biased in the near term, reflecting sticky inflation and a data-dependent Federal Reserve. However, the medium-term trajectory continues to point toward eventual policy easing contingent on a clearer moderation in growth and inflation dynamics.

Latest China’s PMI numbers still show an expansionary manufacturing backdrop, but fragility remains. Non-MFG PMI declined to 49.4, the lowest print since Dec 2022 (excluding Jan 2026 print of 49.4). Note MSCI China has underperformed global benchmarks, with recent equity and bond flows fairly lacklustre into March. In the Shanghai Composite Index, YTD’s biggest losers are financials and consumer names.

Strategy for the month

We continue to favor global equities, particularly the U.S., supported by the resilience of the U.S. economy, strong domestic consumption, and its position as a major energy producer and net exporter. Recent de-escalation in U.S.–Iran tensions has also helped improve global risk sentiment and eased concerns over a prolonged energy shock. More importantly, the U.S. market remains home to world-leading companies with strong earnings visibility, particularly in the technology sector. While valuations are stretched, they are supported by robust earnings growth, rising AI-related capital expenditure from hyperscalers, and continued strong results and guidance from leading AI beneficiaries across semiconductors, cloud computing, and digital infrastructure reinforcing the structural growth outlook for the sector.

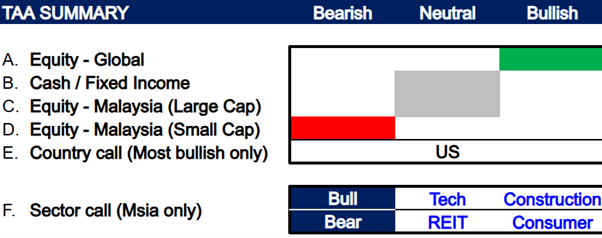

In Malaysia, we maintain a neutral view on large-cap equities and remain bearish on small-cap equities. Sector-wise, we continue to overweight Technology and Construction, supported by ongoing structural digitalisation trends, as well as Malaysia’s established role in the global semiconductor supply chain, alongside broader supply chain diversification under the “China+1” strategy across manufacturing and electronics-related industries. Construction sector is expected to benefit from sustained infrastructure-related demand, including data centre development and power grid upgrades, driven by the broader transition toward cleaner energy and expanding digital infrastructure needs. Meanwhile, we are bearish on REITs (potential pressure from higher interest rates amid lingering inflation concerns), and Consumer sector (pressure from elevated input costs driven by global energy prices and ongoing supply chain disruptions).

Exhibit 2: PCM’s monthly strategy snapshot

Source: PCM, 30 April 2026

Phillip Capital Malaysia and our offerings

We reaffirm our belief that there are still opportunities in the market, and we maintain a discerning approach in choosing high-quality stocks for our portfolio. However, it is crucial to exercise caution and carefully select investment options to ensure the best risk-adjusted returns. By taking a vigilant and discerning approach, investors can potentially reap the benefits of the current market opportunities while minimising risks.

A noteworthy avenue for investors seeking diversification in their portfolio is through PhillipCapital Malaysia. PhillipCapital Malaysia offers multiple private mandate services managed by professional fund managers. By leveraging PhillipCapital Malaysia’s private mandate services, investors can enhance their resiliency, optimise portfolio performance, and navigate the complexities of the market with confidence.

We also offer both conventional and Shariah-compliant options to cater to the needs of all investors. For Malaysia’s mandates, we like:

1. PMART/PMA Dividend Enhanced and/or PMART/PMA Dividend Enhanced ESG

Our PMART Dividend Enhanced and PMA Dividend Enhanced is an income-driven portfolio focused on high dividend-yielding equities. We apply the Dog of the Dow approach, screen and select top market cap stocks to minimise risk and ensure consistent performance. The portfolio is an equal weighting portfolio which reduces concentration risk and provides similar exposure to all clients, both initially and after rebalancing. We offer both conventional and Shariah investment options to cater to the diverse needs of our investors. Click here to learn more. We recently also introduced PMART/PMA Dividend Enhanced ESG Mandate as we remain dedicated to investing in ESG stocks given their stronger valuation and profitability.

2. PMART/PMA ESG

Phillip Capital Malaysia offers discretionary portfolio that invests in stocks with high ESG ratings from the F4GBM and F4GBMS Indices, namely PMART and PMA ESG. There are both conventional and Shariah options available. To explore the companies in which both Conventional and Shariah ESG mandates invest, you can refer to the provided link.

3. PMART/PMA Blue Chip and Opportunity

Our Blue-Chip portfolios primarily allocate our investments towards companies with large market capitalisations, while the Opportunity portfolios predominantly invest in companies with smaller market capitalisations. We also offer both conventional and Shariah-compliant options to cater to the needs of all investors.

Please click on the link to learn more or email us at cse.my@phillipcapital.com.my if you require any further information.

Disclaimer

The information contained herein does not constitute an offer, invitation, or solicitation to invest in any product or service offered by Phillip Capital Management Sdn Bhd (“PCM”). No part of this document may be reproduced or circulated without prior written consent from PCM. This is not a unit trust or collective investment scheme and is not an obligation of, deposit in, or guaranteed by PCM. All investments carry risks, including the potential loss of principal.

Performance figures presented may reflect model portfolios and may differ from actual client accounts’ performance. Variations in individual clients’ portfolios against model portfolios and between one client’s portfolio to another can arise due to multiple factors, including (but not limited to) higher relative brokerage costs for smaller portfolios, timing of capital injections or withdrawals, timing of purchases and sales, and mandate change (e.g., Shariah vs. conventional). These differences may impact overall performance.

Past performance is not necessarily indicative of future returns. The value of investments may rise or fall, and returns are not guaranteed. PCM has not considered your investment objectives, financial situation, or particular needs. You are advised to consult a licensed financial adviser before making any investment decisions.

While all reasonable care has been taken to ensure the accuracy and completeness of the information contained herein, no representation or warranty is made, and no liability is accepted for any loss arising directly or indirectly from reliance on this material. This publication has not been reviewed by the Securities Commission Malaysia.

{kind=link}