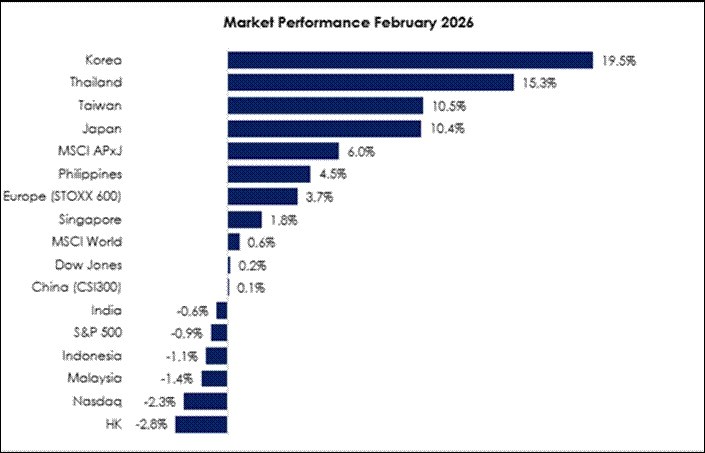

The MSCI Asia Pacific Ex-Japan Index (+6.0%) continued to trump the MSCI World Index (+0.6%) as chipmakers thrive while big tech takes a dive. South Korea (+19.5%) maintained its top performer streak for 3 months in-a-row as the large cap memory plays continue to be the center of investors’ attention. Thailand (+15.3%) was a surprise winner for the month as the Bhumjaithai party’s victory in the recent general elections restored faith to the equity markets. Taiwan (+10.5%) continues to trail South Korea as a prominent foundry in the ongoing booming memory supply chain. Meanwhile, Hong Kong (-2.8%) pulled back some of January’s gains, facing its biggest drop since October last year. Malaysia (-1.4%) endured a slight decline on profit-taking activities after President Trump renewed tariff concerns amidst a jittery global backdrop. Indonesia (-1.1%) remains troubled with a looming MSCI downgrade despite reporting its fastest GDP growth rate in 3 years.

Exhibit 1: Market Performance February 2026

Source: Bloomberg, PCM, 28 February 2026

On the monetary policy front, the People’s Bank of China (PBoC) held its 1-year and 5-year loan prime rates at 3.0% and 3.5%, respectively. The Reserve Bank of India (RBI) maintained its key repo rate at 5.25% during its February meeting, the first monetary policy decision of the year, after cutting it by 25 bps at the December meeting. Within ASEAN, The Bank of Thailand (BoT) unexpectedly cut its key interest rate by 25 basis points to 1.00% at its first review of the year in February. Bank Indonesia kept its benchmark interest rate unchanged at 4.75% for the fifth consecutive meeting in February 2026.

The FBMKLCI Index declined by 1.4% month-on-month (m-o-m) in February, closing at 1,716.61 points. Meanwhile, the FBM Hijrah Shariah Index declined by 0.7% in February, the Mid 70 Index rose by 0.2%, while the Small Cap Index declined by 1.5%. Sector-wise in February, the top-performing sectors were Transport, Property, and Healthcare, which rose by 2.2%, 2.0%, and 0.5% m-o-m, respectively. The worst-performing sectors were Telco, Industrial, and Utilities, which declined by 3.3%, 2.7%, and 2.4% m-o-m, respectively. Within the KLCI, the top three gainers for February were Sime Darby Bhd (+13.0%), Petronas Dagangan Bhd (+3.7%), and Tenaga Nasional Bhd (+3.2%). Meanwhile, the top three decliners for the month were 99 Speed Mart Retail Holdings Bhd (-14.0%), YTL Power International Bhd (-12.4%), and YTL Corporation Bhd (-11.5%).

Foreign investors were net buyers, with a net inflow of RM171.3 million, bringing the year-to-date (YTD) inflows to RM1.2 billion. Separately, in February, there was one listing on the Main Market (Hock Soon Capital Bhd), three listings on the ACE Market (Ambest Grp Bhd, Kee Ming Grp Bhd, and Teamstar Bhd), and two listings on the LEAP Market (Bentley Music Grp Berhad and Whitman Holdings Bhd).

For the month of February, WTI crude oil rose by 2.8% m-o-m, closing at US$67.02 per barrel, while Brent crude oil rose by 2.5% m-o-m, closing at US$72.48 per barrel. Crude palm oil closed at RM3,989/MT, down 4.1% from the previous month, while spot gold rose by 11.3%, ending the month at US$5,247.9/oz. Currency-wise, the Malaysian ringgit appreciated by 1.3% m-o-m against the greenback to RM3.8925/USD. Meanwhile, the Dollar Index rose by 0.6%, ending at 97.6 points.

Equity Market Outlook & Investment Strategy

Malaysia

4Q2025 results were broadly in line overall. Outperformers were mainly seen in Healthcare, selected Consumer names, Utilities and Property. Underperformers were concentrated in Construction, Industrial, Telecommunications & Media, and parts of Technology, reflecting margin and demand pressures. On a separate note, we view the conflict between the United States, Israel and Iran presents second-order impacts to Malaysia – transmitted largely via oil prices and capital flows. Malaysia’s direct trade exposure to Iran remains structurally minimal. We remain focused on domestically oriented sectors, as well as quality and dividend-paying stocks.

Regional

Tensions between the United States, Israel and Iran have escalated significantly during Donald Trump’s second presidency. The first major escalation happened in June 2025, when Israel launched large-scale strikes on Iran’s nuclear and military facilities. Iran responded with waves of missiles and drones targeting Israel, leading to a brief 12-day conflict. The US later joined with strikes on Iranian nuclear sites, showing its willingness to directly intervene to curb Iran’s nuclear ambitions. The confrontation flared up again in February 2026, when the US and Israel carried out another coordinated round of strikes on Iranian military and leadership targets. While markets usually react with short-term fear, we believe the most likely outcome is a prolonged period of ongoing conflict rather than a full-scale war. In this environment, a barbell strategy balancing high-quality growth exposures with income-oriented assets remains well suited to navigating bouts of volatility.

Fixed Income Outlook & Strategy

Malaysia

Malaysian Government Securities (MGS) and Government Investment Issues (GII) are expected to remain range-bound, supported by strong domestic fundamentals, including robust January exports (+19.6% YoY), stable inflation (1.6% YoY), and solid 4Q25 GDP growth (+6.3% YoY). Investor appetite, particularly from domestic institutions, remains healthy, while foreign flows are moderate. External factors, such as tariff uncertainties and regional bond movements, may introduce volatility, but domestic demand and liquidity should anchor yields, with direction guided by upcoming trade, labor, and inflation data, as well as U.S. Treasury yields and Fed policy signals.

Regional

U.S. Treasury yields compressed in February, with the 10-year declining from 4.18% to 4.00%, reflecting a combination of signals of decelerating growth and elevated geopolitical risk premia. Softer 4Q25 GDP, weakening forward-looking indicators (housing, business output, and jobless claims), and rising labour market slack reinforced the late-cycle moderation thesis, prompting renewed demand for duration. Although producer price inflation surprised to the upside for a second consecutive month and January FOMC minutes revealed policy divergence, including conditional openness to further tightening should disinflation stall, market pricing continues to skew toward a July rate cut, suggesting investors view growth risks as increasingly dominant relative to residual inflation pressures. Concurrently, renewed tariff rhetoric under President Trump and intensifying Middle East tensions have sustained safe-haven flows, anchoring yields despite persistent fiscal and trade-related uncertainty.

China’s inbound FDI fell 5.7% YoY to CNY 92.01 billion in January 2026, extending December’s decline and reflecting ongoing investor caution amid structural headwinds and geopolitical uncertainty. Despite weaker aggregate inflows, newly established foreign-invested enterprises rose 25.5%, indicating continued interest in entry, particularly in higher-value-added segments, with high-tech industries accounting for 36.7% of total FDI. Investment remained concentrated in services and manufacturing, while inflows from Germany, Switzerland, and Singapore strengthened. Meanwhile, the People’s Bank of China kept its benchmark lending rates unchanged, with the one-year loan prime rate at 3.0% and the five-year LPR at 3.5%, signaling a measured policy stance that balances growth support with financial stability considerations as authorities preserve room for calibrated easing later in the year.

In February, Japan’s 10-year JGB yield traded in a volatile but contained range of roughly 2.10%–2.27%, ultimately easing toward 2.13% by month-end as growth concerns and moderating inflation offset intermittent hawkish signals. Early upward pressure followed Prime Minister Sanae Takaichi’s electoral mandate for expansionary fiscal policy, but softer 4Q GDP (0.1% QoQ) and cooling inflation, with headline CPI slowing to 1.5%, reinforced demand for duration. Safe-haven flows linked to renewed U.S. tariff threats also weighed on yields. Mid-to-late month, hawkish commentary from Bank of Japan board member Hajime Takata and the appointment of reflation-leaning academics introduced policy uncertainty, prompting brief yield rebounds. Overall, markets remained finely balanced between gradual monetary normalization expectations and a still-fragile macro backdrop.

Strategy for the month

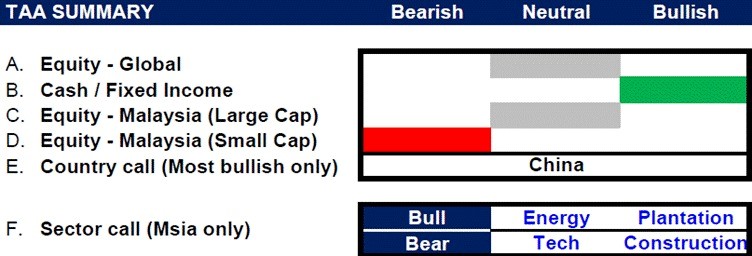

We remain neutral on global equities, mainly the US, as elevated valuations and heavy concentration in a few mega-cap technology names limit broad market upside despite still-robust earnings growth. However, we remain constructive on Asia Pacific ex-Japan equities, particularly in North Asia, supported by a weaker US dollar and a more dovish Federal Reserve. Further easing by the Fed would give Asian central banks greater flexibility to lower interest rates, which in turn could further support regional market sentiment.

In Malaysia, we are maintaining our neutral view on large-cap equities and remain bearish on small-cap equities. Sector-wise, we turned overweight in the Energy and Plantation sectors due to the rising in commodity prices as a result of the logistics crunch in the Strait of Hormuz. Meanwhile, we maintain our bearish view for Construction (muted near-term construction billings) and Tech sector (lack of exposure to the AI boom and US trade protectionism)

Exhibit 2: PCM’s monthly strategy snapshot

Source: PCM, 28 February 2026

Phillip Capital Malaysia and our offerings

We reaffirm our belief that there are still opportunities in the market, and we maintain a discerning approach in choosing high-quality stocks for our portfolio. However, it is crucial to exercise caution and carefully select investment options to ensure the best risk-adjusted returns. By taking a vigilant and discerning approach, investors can potentially reap the benefits of the current market opportunities while minimising risks.

A noteworthy avenue for investors seeking diversification in their portfolio is through PhillipCapital Malaysia. PhillipCapital Malaysia offers multiple private mandate services managed by professional fund managers. By leveraging PhillipCapital Malaysia’s private mandate services, investors can enhance their resiliency, optimise portfolio performance, and navigate the complexities of the market with confidence.

We also offer both conventional and Shariah-compliant options to cater to the needs of all investors. For Malaysia’s mandates, we like:

1. PMART/PMA Dividend Enhanced and/or PMART/PMA Dividend Enhanced ESG

Our PMART Dividend Enhanced and PMA Dividend Enhanced is an income-driven portfolio focused on high dividend-yielding equities. We apply the Dog of the Dow approach, screen and select top market cap stocks to minimise risk and ensure consistent performance. The portfolio is an equal weighting portfolio which reduces concentration risk and provides similar exposure to all clients, both initially and after rebalancing. We offer both conventional and Shariah investment options to cater to the diverse needs of our investors. Click here to learn more. We recently also introduced PMART/PMA Dividend Enhanced ESG Mandate as we remain dedicated to investing in ESG stocks given their stronger valuation and profitability.

2. PMART/PMA ESG

Phillip Capital Malaysia offers discretionary portfolio that invests in stocks with high ESG ratings from the F4GBM and F4GBMS Indices, namely PMART and PMA ESG. There are both conventional and Shariah options available. To explore the companies in which both Conventional and Shariah ESG mandates invest, you can refer to the provided link.

3. PMART/PMA Blue Chip and Opportunity

Our Blue-Chip portfolios primarily allocate our investments towards companies with large market capitalisations, while the Opportunity portfolios predominantly invest in companies with smaller market capitalisations. We also offer both conventional and Shariah-compliant options to cater to the needs of all investors.

Please click on the link to learn more or email us at cse.my@phillipcapital.com.my if you require any further information.

{kind=link}