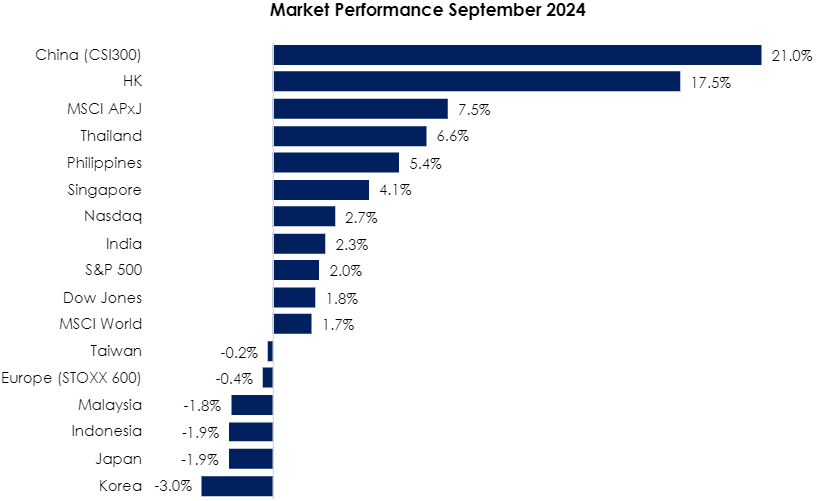

The MSCI Asia Pacific Ex-Japan Index (+7.5%) blew past the MSCI World Index (+1.7%) mom in September as a slew of much needed policy catalysts finally materialised to aid China ailing economy. China (+21.0%) and Hong Kong (+17.5%) were breakout stars for the month after the PBOC announced a wealth of monetary stimulus measures including cutting banks reserve ratio, reducing policy rates and various initiatives to prop up China long distressed property market. Thailand (+6.6%) performed splendidly in their own right as foreign investors flock back into the country attributed to a favourable view on the nation’s policy direction and fiscal stimulus measures. Moving focus towards the decliners, South Korea (-3.0%) market loses steam as the semiconductor cycle reaches the late phase but latest positive industrial output data may support the view that the chip rally has more room to go. Japan (-1.9%) fell swiftly after the election of the new Prime Minister Shigeru Ishiba as a knee-jerk reaction amid policy uncertainty. Indonesia (-1.9%) also faced sudden decline as Barito Renewables Energy, the nation 2nd largest company, dropped >30% in the month on news of FTSE Russell exclusion (see Exhibit 1).

Exhibit 1: Market Performance Sep 2024

Source: Bloomberg, PCM, 30 Sep 2024

In the US, the Fed lowered interest rates by 50bps, bringing the benchmark rate to 4.75%-5.00%. Back to China, while the one-year loan prime rate (LPR) was kept at 3.35%, and the five-year LPR was unchanged at 3.85%, the People’s Bank of China (PBoC) announced a 20bps cut to the 7-day repo rate and a 50bps cut in the Reserve Requirement Ratio (RRR), with the potential for an additional cut of 25 to 50bps by year-end.

Back home, FBMKLCI fell 1.8% mom in September and closed at 1,648.91. Similarly, Small Cap Index fell by 0.6% and the Mid 70 Index decreased by 0.3%. Sector-wise, the top performers were Healthcare, Construction and Property, with gains of 6.9%, 5.2% and 4.2% mom, respectively. Laggards were Energy, Technology and Telco, declining by -8.7%, -7.3%, and -3.1% mom, respectively. In terms of fund flow, foreign investors stayed net buyers for the third consecutive month in September, with net inflow of RM0.5bn. This brings the cumulative net inflow for the first nine months of 2024 to RM3.6bn.

Strategy for the month

The series of measures announced in September in China primarily focus on monetary policy. For a more sustainable rebound, we believe policymakers should also enhance fiscal policy initiatives and take more decisive action to tackle excess housing inventory. Despite the recent rally, as of 30 September 2024, the Hang Seng Index is trading at a forward P/E ratio of 9.2x, remaining below its five-year historical median of 10.5x. That said, investors need to watch the upcoming US presidential election as it may bring renewed uncertainty to Sino-US relation.

Back home, following a 38% depreciation of the ringgit from below RM3.00/USD in May 2013 to RM4.80/USD in April 2024, the trend appears to have shifted decisively. As of 30 September 2024, the exchange rate had improved to RM4.12/USD, representing a 14% increase from this year’s low. We believe the reflationary effects on domestic risk assets, such as equities and real estate, will be significant. We remain optimistic about Malaysia, supported by a weak dollar, strong domestic corporate earnings growth, and additional policy catalysts, including consumption boosts, fiscal consolidation, and project rollouts. Key upcoming events include the tabling of Budget 2025 on 18 October.

In terms of market positioning, our preference in order is: Malaysia (policy) > US (earnings resiliency) > Asia Pacific excluding Japan = Emerging Markets (benefiting from rate cuts) > China (valuation). Furthermore, we believe Malaysia is well positioned to navigate external uncertainties, buoyed by strong economic growth and there are numerous promising themes in the market for investment at this time.

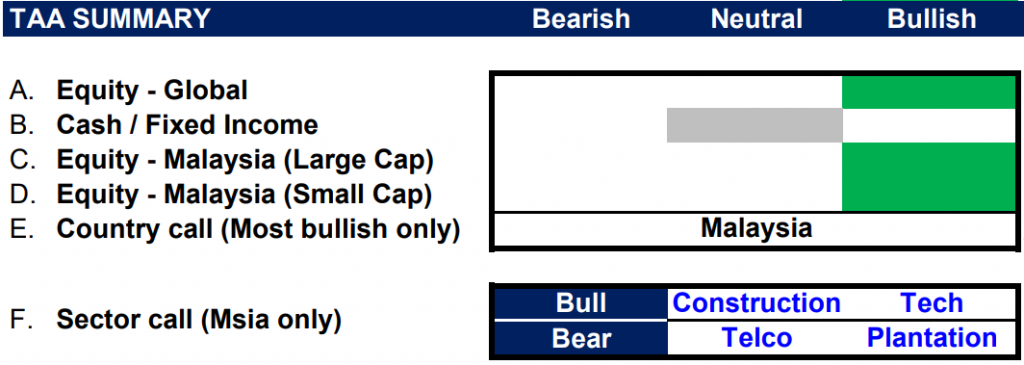

In Malaysia, we favour large-cap stocks and selected small-cap stocks. Sector-wise, we favour the Construction sector due to project rollouts and data center investments, and the Technology sector as semiconductor stabilization and AI opportunities emerge. We are also optimistic about the Consumer sector from pension hikes and EPF Account 3 withdrawals, as well as the Finance sector, driven by improvements in both interest and non-interest income. Conversely, we continue to hold our underweight stance in Telco and Plantation sectors (see Exhibit 2).

Exhibit 2: PCM’s monthly strategy snapshot

Source: PCM, 30 Sep 2024

We will share our comments on Budget 2025 in a separate piece.

Phillip Capital Malaysia and our offerings

We reaffirm our belief that there are still opportunities in the market, and we maintain a discerning approach in choosing high-quality stocks for our portfolio. However, it is crucial to exercise caution and carefully select investment options to ensure the best risk-adjusted returns. By taking a vigilant and discerning approach, investors can potentially reap the benefits of the current market opportunities while minimising risks.

A noteworthy avenue for investors seeking diversification in their portfolio is through PhillipCapital Malaysia. PhillipCapital Malaysia offers multiple private mandate services managed by professional fund managers. By leveraging PhillipCapital Malaysia’s private mandate services, investors can enhance their resiliency, optimise portfolio performance, and navigate the complexities of the market with confidence.

We also offer both conventional and Shariah-compliant options to cater to the needs of all investors. For Malaysia’s mandates, we like:

- PMART/PMA Dividend Enhanced and/or PMART/PMA Dividend Enhanced ESG

Our PMART Dividend Enhanced and PMA Dividend Enhanced is an income-driven portfolio focused on high dividend-yielding equities. We apply the Dog of the Dow approach, screen and select top market cap stocks to minimise risk and ensure consistent performance. The portfolio is an equal weighting portfolio which reduces concentration risk and provides similar exposure to all clients, both initially and after rebalancing. We offer both conventional and Shariah investment options to cater to the diverse needs of our investors. Click here to learn more. We recently also introduced PMART/PMA Dividend Enhanced ESG Mandate as we remain dedicated to investing in ESG stocks given their stronger valuation and profitability.

- PMART/PMA ESG

Phillip Capital Malaysia offers discretionary portfolio that invests in stocks with high ESG ratings from the F4GBM and F4GBMS Indices, namely PMART and PMA ESG. There are both conventional and Shariah options available. To explore the companies in which both Conventional and Shariah ESG mandates invest, you can refer to the provided link.

- PMART/PMA Blue Chip and Opportunity

Our Blue-Chip portfolios primarily allocate our investments towards companies with large market capitalisations, while the Opportunity portfolios predominantly invest in companies with smaller market capitalisations. We also offer both conventional and Shariah-compliant options to cater to the needs of all investors.

Please click on the link to learn more or email us at cse.my@phillipcapital.com.my if you require any further information.

Disclaimer:

The information contained herein does not constitute an offer, invitation or solicitation to invest in Phillip Capital Management Sdn Bhd (“PCM”). This article has been reviewed and endorsed by the Executive Director (ED) of PCM. This article has not been reviewed by The Securities Commission Malaysia (SC). No part of this document may be circulated or reproduced without prior permission of PCM. This is not a collective investment scheme / unit trust fund. Any investment product or service offered by PCM is not obligations of, deposits in or guaranteed by PCM. Past performance is not necessarily indicative of future returns. Investments are subject to investment risks, including the possible loss of the principal amount invested. Investors should note that the value of the investment may rise as well as decline. If investors are in any doubt about any feature or nature of the investment, they should consult PCM to obtain further information including on the fees and charges involved before investing or seek other professional advice for their specific investment needs or financial situations. Whilst we have taken all reasonable care to ensure that the information contained in this publication is accurate, it does not guarantee the accuracy or completeness of this publication. Any information, opinion and views contained herein are subject to change without notice. We have not given any consideration to and have not made any investigation on your investment objectives, financial situation or your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any persons acting on such information and advice.

{kind=link}