In our earlier piece, we discussed how ESG stocks tend to enjoy stronger valuation and profitability, attributed to their adept risk management, innovative operational efficiencies, alignment with regulatory compliance, and enhanced reputation and brand equity, fostering higher shareholder returns and better profitability.

Indeed, according to Bloomberg’s consensus data, the KLCI is projected to witness earnings growth of 8.01% in 2024. However, the FTSE4Good Bursa Malaysia Index (F4GBM) is anticipated to experience growth of 13.29%, while the FTSE4Good Bursa Malaysia Shariah Index (F4GBMS) is forecasted to grow by 19.83%. The KLCI, predominantly comprising traditional sectors like Financials, Plantations, Telecommunications, and Utilities, exhibits slower earnings growth. Conversely, the F4GBM Index and F4GBMS Index, as of the latest review in December 2023, consist of 109 and 88 constituents respectively, including growth sectors like Manufacturing, Industrial, and Technology, thereby explaining their robust earnings growth.

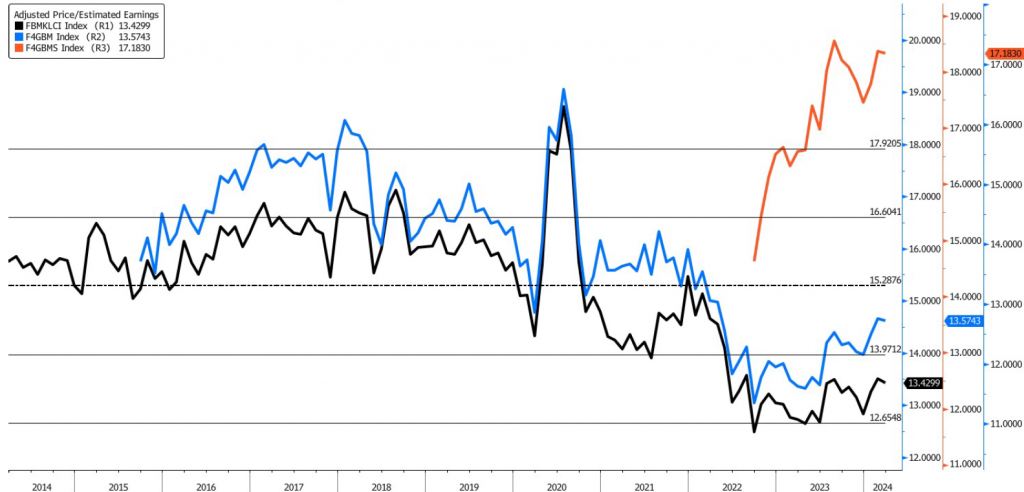

This variance in earnings growth helps explain why the price-to-earnings (PE) ratios of the F4GBM Index (13.57x) and F4GBMS Index (17.18x) trade at a premium compared to the KLCI (13.43x). Notably, the F4GBMS Index commands a higher PE primarily because it excludes banking stocks, which typically trade at lower PEs due to their mature business nature, thereby influencing the overall valuation dynamics (see Exhibit 1).

Exhibit 1: 10-Year Valuation Chart (FBMKLCI, F4GBM, F4GBMS)

Source: Bloomberg, PCM, 20 March 2024

Note: The F4GBM and F4GBMS Index were introduced in December 2014 and July 2021, respectively.

This could possibly explain why our ESG mandates demonstrated robust performance in 2023, achieving a significant positive return of +9.70%. This performance surpassed the KLCI, which experienced a decline of -2.73%, and exceeded the F4GBM Index, which saw a modest increase of +0.67%, while the F4GBMS Index declined marginally by -0.29%. This favourable performance extended into 2024, with our ESG mandates recording a return of 5.45%, aligning closely with the KLCI’s 6.65% and the F4GBM Index’s 6.07%, while the F4GBMS Index achieved a return of 5.07%. Our ESG Mandates come in both conventional and Shariah options, catering to investors seeking to optimise the risk-adjusted return by constructing a diverse sustainable portfolio of ESG companies.

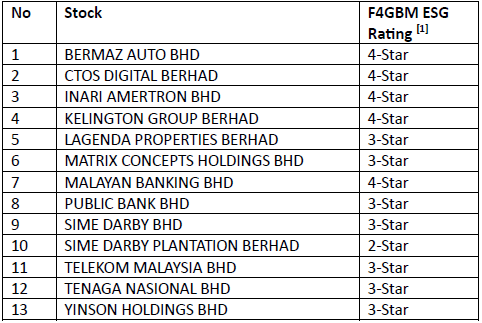

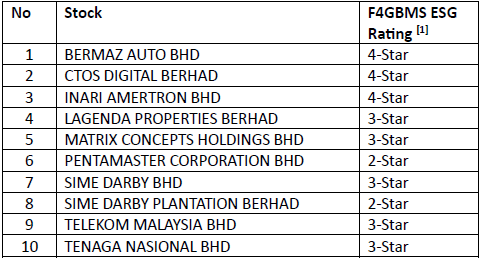

Here is the list of stocks in our ESG mandates.

Table 1: ESG Mandates – Stock List 2024

Conventional ESG Portfolio

Shariah ESG Portfolio

Source: PCM

How our holdings could harness the benefits of increasing ESG trend?

We believe listed companies with good ESG practices will continue to benefit from the rising sustainability trend. Furthermore, we have pinpointed selected names within key sectors—Construction, Renewables, Utilities, and Property—that stand to benefit from the Net-Zero Transition Roadmap (NETR) and the policies outlined in Budget 2024. As companies enhance their ESG performance, we foresee a reduction in the risks associated with foreign labour dependency, a factor that historically affected industries such as Plantation, Construction, Gloves, and Electronic Manufacturing Services (EMS). With supply chains increasingly prioritising ESG criteria, ongoing government and corporate initiatives will help mitigate the risks of sanctions and reputational damage. This is crucial amid heightened ESG scrutiny, safeguarding trade opportunities.

We will consistently assess our holdings and adjust our portfolio as necessary to align with prevailing market conditions. Please click on the link to learn more or email us at cse.my@phillipcapital.com.my if you require any further information.

Note:

[1] ESG Ratings of Public Listed Companies (PLCs) assessed by FTSE Russell in accordance with FTSE Russell ESG Ratings Methodology, December 2023 – link

Disclaimer:

The information contained herein does not constitute an offer, invitation or solicitation to invest in Phillip Capital Management Sdn Bhd (“PCM”). This article has been reviewed and endorsed by the Executive Director (ED) of PCM. This article has not been reviewed by The Securities Commission Malaysia (SC). No part of this document may be circulated or reproduced without prior permission of PCM. This is not a collective investment scheme / unit trust fund. Any investment product or service offered by PCM is not obligations of, deposits in or guaranteed by PCM. Past performance is not necessarily indicative of future returns. Investments are subject to investment risks, including the possible loss of the principal amount invested. Investors should note that the value of the investment may rise as well as decline. If investors are in any doubt about any feature or nature of the investment, they should consult PCM to obtain further information including on the fees and charges involved before investing or seek other professional advice for their specific investment needs or financial situations. Whilst we have taken all reasonable care to ensure that the information contained in this publication is accurate, it does not guarantee the accuracy or completeness of this publication. Any information, opinion and views contained herein are subject to change without notice. We have not given any consideration to and have not made any investigation on your investment objectives, financial situation or your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any persons acting on such information and advice.

{kind=link}