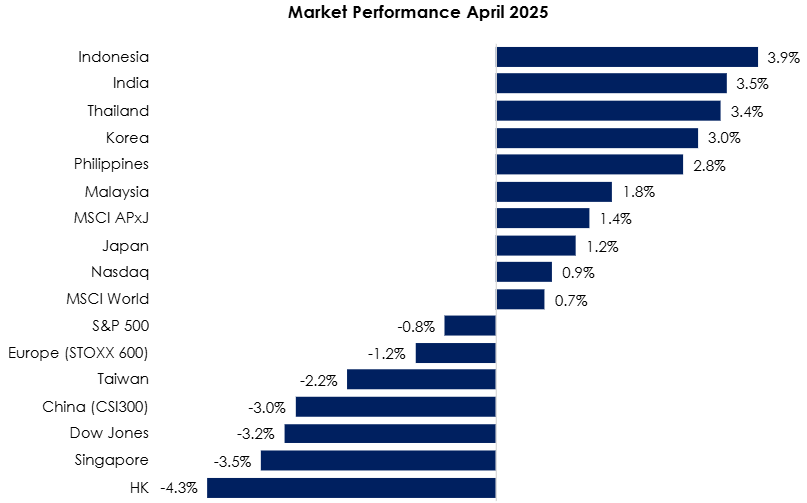

The MSCI Asia Pacific Ex-Japan Index (+1.4%) continued to outperform the MSCI World Index (+0.7%) for the third month in a row, as US and European markets were still stumbling from the aftereffects of Trump’s radical trade protectionism stance. Indonesia (+3.9%) continued its strong rally since March, retracing most of the losses from February’s political-fuelled selloff. India (+3.5%) posted robust gains, driven by renewed foreign investor interest. Thailand (+3.4%) rebounded fairly after plunging to near-Covid lows, an indication of severe uncertainty over the structural change threatening Thailand’s once-vibrant manufacturing base. On the other side of the trade war, HK (-4.3%) and China (-3.0%) struggled as foreign funds pulled out heavily on escalating trade war tensions. Singapore (-3.5%) was no stranger to Trump’s tariff selloff, prompting MAS to ease its monetary policy for the 2nd consecutive time since its January meeting (see Exhibit 1).

Exhibit 1: Market Performance April 2025

Source: Bloomberg, PCM, 30 April 2025

On the monetary policy front, in April, the European Central Bank (ECB) lowered interest rates by 25 basis points to 2.25%, marking the third cut this year. In Asia, the Reserve Bank of India cut its policy rate by 25 basis points to 6.00%, the second rate cut this year. Within ASEAN, the Philippine central bank lowered its benchmark interest rate by 25 basis points to 5.50%, while the Bank of Thailand reduced its policy rate by 25 basis points to 1.75%. The Monetary Authority of Singapore (MAS) also announced a slight reduction in the rate of appreciation of the Singapore dollar nominal effective exchange rate (S$NEER) policy band. The width of the band and its centre remained unchanged.

The FBMKLCI gained 1.8% mom in April, closing at 1,540.22, with much of the upward momentum occurring on the final trading day of the month. In contrast, the Small Cap Index fell by 1.6%, while the Mid 70 Index decreased by 2.0%. Sector-wise in April, the top performing sectors were Telecommunications, Consumer, and Healthcare, up 4.8%, 4.1%, and 2.9% respectively. The worst performing sectors were Energy, Transport, and Technology, which saw declines of 9.8%, 5.2%, and 5.1%, respectively. Foreign investors continued to be net sellers for the seventh consecutive month in April, recording net sell flows of RM1.9bn, with outflows totaling RM19.6bn over the past seven months.

Equity Market Outlook & Investment Strategy

Malaysia

The present market volatility and uncertainties are not over yet despite the recent positive developments in US-China tariff policies that support a risk-on sentiment. While the market provides investment opportunities for those with cash and holding power, heightened market risk is still ongoing. Near-term market direction remains closely tied to the progress of US tariff negotiations with key trading partners, including Malaysia. Meanwhile, investors face a complex mix of headwinds: US-China tensions, rising recession risks, Fed policy uncertainty, the ongoing US earnings season, and Malaysia’s upcoming May reporting cycle. That said, valuations remain attractive, with the KLCI trading at 12.7x P/E—approximately 25% below its 10-year mean of 17x. Additionally, foreign shareholding remains near historic lows at 19.4% (as of April), signalling potential upside from further positioning flows.

Regional

Global equities may encounter near-term challenges due to escalating geopolitical tensions, persistent inflation, and slower global growth. While some central banks have initiated rate cuts, the U.S. Federal Reserve has yet to follow suit. Markets anticipate a potential rate cut in June to support U.S. growth, especially after the economy contracted at an annualized rate of 0.3% in Q1 2025—the first decline since early 2022. While rate cuts may support valuations, trade uncertainties and uneven growth across regions could weigh on sentiment. As global markets grapple with heightened uncertainty, we emphasize the importance of diversification and a focus on quality amid volatility

Fixed Income Outlook & Strategy

Malaysia

Renewed optimism surrounding US-China trade talks improved investor sentiment and contributed to a broad-based rally in local bonds. This was further supported by signs of weakness in the US economy, which placed downward pressure on global yields and enhanced the attractiveness of local debt. Domestically, positive trade momentum and deepening bilateral ties with countries such as Maldives, Japan, Italy, and Vietnam helped set a constructive tone for investment.

We maintain our view that BNM will keep the Overnight Policy Rate (OPR) at 3.0% in the May MPC meeting. We continue to overweight corporate bonds over MGS/GII due to higher yields.

Regional

The 10-year US Treasury yield saw sharp swings in April 2025, reflecting heightened market sensitivity to shifting trade and policy signals. It initially dropped to 3.86% on April 4, the lowest level since October 2024, driven by growing expectations of the Federal Reserve easing after President Trump reiterated his hardline tariff stance, which stoked fears of slower economic growth. However, yields reversed course and climbed toward 4.50% after Trump unexpectedly announced a 90-day pause on the US tariffs, excluding China. Rather than calming markets, the abrupt shift triggered a broad sell-off in the US equities and outflows from dollar assets, as investors interpreted the move as further evidence of erratic policymaking. The resulting uncertainty deepened market unease, reinforcing concerns about the sustainability of both the policy outlook and global risk sentiment.

In China, the strong growth in the industrial sector due to frontloading activities continued to drive China economic outperformance in 1Q25. Retail sales and urban fixed asset investment (FAI) also came in above expectations in March, and the national survey jobless rate eased back to 5.2%

In April 2025, the European Central Bank (ECB) implemented a 25bp interest rate cut in response to growing economic headwinds from global trade tensions, which have eroded business confidence and weakened trade activity across the eurozone. Effective 23 April 2025, the ECB lowered the deposit facility rate to 2.25%, the main refinancing operations rate to 2.40%, and the marginal lending facility rate to 2.65%. The decision reflects the ECB’s concerns over slowing growth and persistent uncertainty, reinforcing its commitment to supporting the eurozone economy through accommodative monetary policy.

Strategy for the month

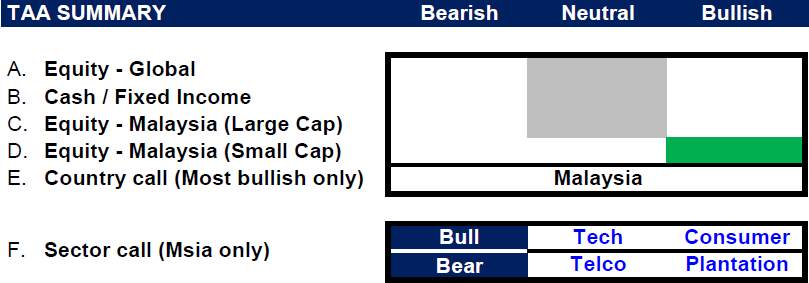

We remain neutral on global equities as geopolitical risks and soft economic data continue to weigh on market sentiment in the near to medium term, though we note positive signs of easing US–China trade tensions. We turned more constructive on Asia Pacific ex-Japan equities as export-driven countries may benefit short term from easing tariff tensions, with North Asia likely to gain momentum.

We continue to prefer Malaysia, supported by its highly domestically oriented economy, attractive valuations, and low levels of foreign shareholding. We maintain a neutral view on large-cap stocks due to balanced risk-reward and have shifted to bullish on small-caps amid recent positive developments in US-China tariff policies that support a risk-on sentiment. Sector-wise, we turn bullish on Technology for the same reason, while continue to prefer selected Consumer stocks for their defensive earnings, easing margin pressures amid a stronger ringgit and lower commodity prices. On the other hand, we maintain an underweight stance on the Telco and Plantation sectors given the lack of catalysts.

Exhibit 2: PCM’s monthly strategy snapshot

Source: PCM, 30 April 2025

Phillip Capital Malaysia and our offerings

We reaffirm our belief that there are still opportunities in the market, and we maintain a discerning approach in choosing high-quality stocks for our portfolio. However, it is crucial to exercise caution and carefully select investment options to ensure the best risk-adjusted returns. By taking a vigilant and discerning approach, investors can potentially reap the benefits of the current market opportunities while minimising risks.

A noteworthy avenue for investors seeking diversification in their portfolio is through PhillipCapital Malaysia. PhillipCapital Malaysia offers multiple private mandate services managed by professional fund managers. By leveraging PhillipCapital Malaysia’s private mandate services, investors can enhance their resiliency, optimise portfolio performance, and navigate the complexities of the market with confidence.

We also offer both conventional and Shariah-compliant options to cater to the needs of all investors. For Malaysia’s mandates, we like:

- PMART/PMA Dividend Enhanced and/or PMART/PMA Dividend Enhanced ESG

Our PMART Dividend Enhanced and PMA Dividend Enhanced is an income-driven portfolio focused on high dividend-yielding equities. We apply the Dog of the Dow approach, screen and select top market cap stocks to minimise risk and ensure consistent performance. The portfolio is an equal weighting portfolio which reduces concentration risk and provides similar exposure to all clients, both initially and after rebalancing. We offer both conventional and Shariah investment options to cater to the diverse needs of our investors. Click here to learn more. We recently also introduced PMART/PMA Dividend Enhanced ESG Mandate as we remain dedicated to investing in ESG stocks given their stronger valuation and profitability.

- PMART/PMA ESG

Phillip Capital Malaysia offers discretionary portfolio that invests in stocks with high ESG ratings from the F4GBM and F4GBMS Indices, namely PMART and PMA ESG. There are both conventional and Shariah options available. To explore the companies in which both Conventional and Shariah ESG mandates invest, you can refer to the provided link.

- PMART/PMA Blue Chip and Opportunity

Our Blue-Chip portfolios primarily allocate our investments towards companies with large market capitalisations, while the Opportunity portfolios predominantly invest in companies with smaller market capitalisations. We also offer both conventional and Shariah-compliant options to cater to the needs of all investors.

Please click on the link to learn more or email us at cse.my@phillipcapital.com.my if you require any further information.

TAA_Presentation_Deck_May-15.5.2025.pdf

Disclaimer:

The information contained herein does not constitute an offer, invitation or solicitation to invest in Phillip Capital Management Sdn Bhd (“PCM”). This article has been reviewed and endorsed by the Executive Director (ED) of PCM. This article has not been reviewed by The Securities Commission Malaysia (SC). No part of this document may be circulated or reproduced without prior permission of PCM. This is not a collective investment scheme / unit trust fund. Any investment product or service offered by PCM is not obligations of, deposits in or guaranteed by PCM. Past performance is not necessarily indicative of future returns. Investments are subject to investment risks, including the possible loss of the principal amount invested. Investors should note that the value of the investment may rise as well as decline. If investors are in any doubt about any feature or nature of the investment, they should consult PCM to obtain further information including on the fees and charges involved before investing or seek other professional advice for their specific investment needs or financial situations. Whilst we have taken all reasonable care to ensure that the information contained in this publication is accurate, it does not guarantee the accuracy or completeness of this publication. Any information, opinion and views contained herein are subject to change without notice. We have not given any consideration to and have not made any investigation on your investment objectives, financial situation or your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any persons acting on such information and advice.

{kind=link}