Market Review (March 2026)

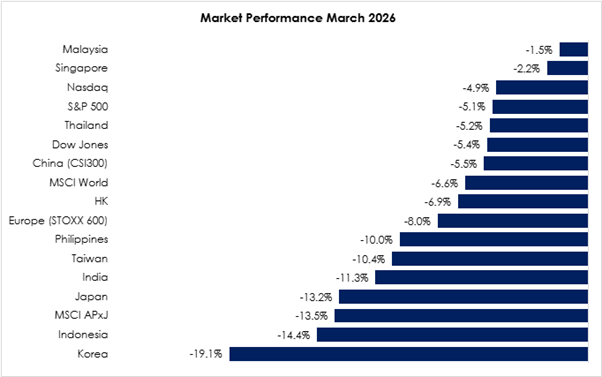

The MSCI Asia Pacific Ex-Japan Index (-13.5%) suffered a devastating selloff compared to the MSCI World Index (-6.6%) with emerging markets taking the brunt of the impact from US & Israel’s war against Iran. No index was spared from the selloff as all major markets registered a decline in March. South Korea (-19.1%) erased all of February’s gains as rising oil prices weighed on the outlook for the energy-import dependent economy, while concerns over Google’s new research development titled TurboQuant—an AI compression algorithm that could significantly reduce memory requirements for large language models—sparked a selloff in memory-related stocks. Indonesia (-14.4%) also tumbled on oil price woes with the government enacting work-from-home mandates for public employees and other initiatives to cut down on fuel consumption. India (-11.3%), the world’s second largest net importer of crude oil, was struck with a double setback, as its rapidly weakening rupee and ballooning input costs hampered its high growth outlook. Malaysia (-1.5%) was the unsung hero of March, as its net energy exporter status helped cushion the decline considerably compared to regional peers.

Exhibit 1: Market Performance March 2026

Source: Bloomberg, PCM, 31 March 2026

On the monetary policy front, the People’s Bank of China (PBoC) maintained its 1-year and 5-year loan prime rates at 3.0% and 3.5%, respectively. The Reserve Bank of Australia (RBA) raised the official cash rate by 25 basis points to 4.10% in March 2026, following a previous hike to 3.85% in February, to combat persistent inflation and strong consumer demand. Within ASEAN, Bank Indonesia maintained its benchmark interest rate at 4.7% for the fifth consecutive meeting in March 2026, while the Bangko Sentral ng Pilipinas kept its policy rate unchanged at 4.25% in an unscheduled meeting on March 23, 2026, following a 25bp cut in February.

The FBMKLCI Index declined by 1.5% month-on-month (m-o-m) in March, closing at 1,690.36 points. Meanwhile, the FBM Hijrah Shariah Index gained by 0.9% in March, the Mid 70 Index declined by 3.8%, while the Small Cap Index slipped by 7.1%. Sector-wise in March, the top-performing sectors were Plantation, Industrial, and Energy, which rose by 8.6%, 7.1%, and 5.8% m-o-m, respectively. The worst-performing sectors were Construction, Technology, and Consumer, which declined by 11.2%, 9.6%, and 8.3% m-o-m, respectively.

Within the KLCI, the top three gainers for March were Petronas Chemicals Group Bhd (+104.6%), Sunway Healthcare Holdings Bhd (+38.0%), and Kuala Lumpur Kepong Bhd (+13.2%). Meanwhile, the top three decliners were Sunway Bhd (-16.3%), Mr D.I.Y. Group (M) Bhd (-13.6%), and Gamuda Bhd (-11.0%).

Foreign investors were net sellers, with a net outflow of RM41.7 million, bringing the year-to-date (YTD) inflows to RM1.2 billion. Separately, in March, there was one listing on the Main Market (Sunway Healthcare Holdings Berhad), two listings on the ACE Market (OGX Group Berhad, Adnex Group Berhad), and one listing on the LEAP Market (Bimoffice Group Berhad).

For the month of March, WTI crude oil rose by 51.3% m-o-m to US$101.4 per barrel, while Brent crude increased by 63.3% m-o-m to US$118.5 per barrel. Crude palm oil rose to RM4,729/MT, up 18.6% from the previous month, while spot gold declined by 11.4% to US$4,647.6/oz. Currency-wise, the Malaysian ringgit depreciated by 3.9% m-o-m against the greenback to RM4.0495/USD. Meanwhile, the Dollar Index rose by 2.4% to 99.9 points.

Equity Market Outlook & Investment Strategy

Malaysia

Malaysia is expected to experience indirect (second-order) effects from the US–Israel–Iran conflict, mainly through a surge in oil prices above USD100 per barrel and shifts in global capital flows. While Malaysia’s direct trade exposure to Iran remains structurally minimal, the government is grappling with a ballooning subsidy bill that may necessitate tighter eligibility for cash transfers. Consequently, we maintain a cautious stance, shifting our focus toward defensive, domestic sectors and high-quality dividend stocks to hedge against energy-driven global volatility.

Regional

Following President Trump’s recent remarks regarding the seizure of Iranian export hubs like Kharg Island, we anticipate further escalation for several weeks before any diplomatic intervention to end the conflict occurs. While markets often react with short-term volatility, we believe this presents opportunities for disciplined, long-term investors. In this environment, a barbell strategy balancing high-quality growth exposures with income-oriented assets remains well suited to navigating bouts of volatility, while incorporating broader diversification to serve as a critical hedge against potential energy shocks.

Fixed Income Outlook & Strategy

Malaysia

MGS yields are expected to trend mildly higher but remain well-anchored, supported by stable domestic fundamentals, contained inflation, and a steady policy stance from Bank Negara Malaysia. While global factors—particularly oil prices and US yields—pose upside risks, continued foreign inflows and macro resilience should limit volatility, keeping the market largely range-bound.

Regional

US Treasury yields repriced higher through March, with the 10-year yield closing near 4.40%, as markets increasingly priced a prolonged higher-for-longer interest rate environment. The shift was underpinned by resilient economic data, firm labour market conditions, and energy-driven inflation risks linked to geopolitical developments. The Federal Reserve kept the Fed Funds Rate unchanged at 3.50%–3.75%, while signalling a more inflation-conscious stance, effectively pushing back expectations for near-term rate cuts. Although intermittent rallies occurred alongside oil price pullbacks, the overall bias remains toward elevated yields, with investors demanding higher term premia amid persistent inflation uncertainty and geopolitical risks.

UST yields are likely to remain elevated and volatile, reflecting persistent inflation risks and a “higher-for-longer” stance from the Federal Reserve. Near-term direction will be driven by energy prices and data, with risks skewed toward higher yields, though growth concerns may cap the upside intermittently.

China’s PMIs rebounded into expansionary territory in March, reflecting a seasonal normalization in activity following the Spring Festival lull, with both manufacturing and services showing sequential improvement. The manufacturing PMI rose to 50.4, supported by stronger production and new orders, indicating resilient industrial momentum, while the non-manufacturing PMI edged up to 50.1, driven by a recovery in services despite continued weakness in construction. Notably, export-related indicators such as port container throughput suggest external demand remained intact during the month. However, a sharp rise in global oil prices has begun to feed into upstream costs, as reflected in the surge in raw material prices, although pass-through to output prices remains partial, pointing to still-fragile downstream demand conditions.

Strategy for the month

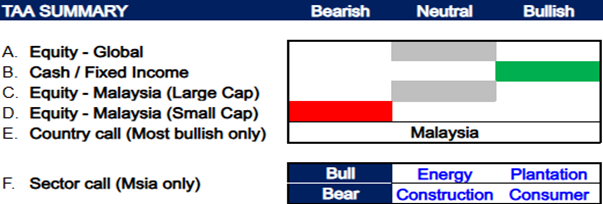

We remain neutral on global equities, mainly the US, as elevated valuations and heavy concentration in a few mega-cap technology names limit broad market upside despite still-robust earnings growth. However, we remain constructive on Malaysian equities, underpinned by their defensive characteristics and resilient domestic demand. This positive stance is further supported by attractive dividend yields and a structural upcycle across key local sectors. Further easing by the Fed would give Asian central banks greater flexibility to lower interest rates, which in turn could further support regional market sentiment.[CKQ1.1]

In Malaysia, we are maintaining our neutral view on large-cap equities and remain bearish on small-cap equities. Sector-wise, we turned overweight in the Energy and Plantation sectors due to the rising in commodity prices as a result of the logistics crunch in the Strait of Hormuz. Meanwhile, we maintain our bearish view for Construction (muted near-term construction billings) and Consumer sector (margin pressure due to elevated costs stemming from geopolitical disruptions).

Exhibit 2: PCM’s monthly strategy snapshot

Source: PCM, 31 March 2026

Phillip Capital Malaysia and our offerings

We reaffirm our belief that there are still opportunities in the market, and we maintain a discerning approach in choosing high-quality stocks for our portfolio. However, it is crucial to exercise caution and carefully select investment options to ensure the best risk-adjusted returns. By taking a vigilant and discerning approach, investors can potentially reap the benefits of the current market opportunities while minimising risks.

A noteworthy avenue for investors seeking diversification in their portfolio is through PhillipCapital Malaysia. PhillipCapital Malaysia offers multiple private mandate services managed by professional fund managers. By leveraging PhillipCapital Malaysia’s private mandate services, investors can enhance their resiliency, optimise portfolio performance, and navigate the complexities of the market with confidence.

We also offer both conventional and Shariah-compliant options to cater to the needs of all investors. For Malaysia’s mandates, we like:

1. PMART/PMA Dividend Enhanced and/or PMART/PMA Dividend Enhanced ESG

Our PMART Dividend Enhanced and PMA Dividend Enhanced is an income-driven portfolio focused on high dividend-yielding equities. We apply the Dog of the Dow approach, screen and select top market cap stocks to minimise risk and ensure consistent performance. The portfolio is an equal weighting portfolio which reduces concentration risk and provides similar exposure to all clients, both initially and after rebalancing. We offer both conventional and Shariah investment options to cater to the diverse needs of our investors. Click here to learn more. We recently also introduced PMART/PMA Dividend Enhanced ESG Mandate as we remain dedicated to investing in ESG stocks given their stronger valuation and profitability.

2. PMART/PMA ESG

Phillip Capital Malaysia offers discretionary portfolio that invests in stocks with high ESG ratings from the F4GBM and F4GBMS Indices, namely PMART and PMA ESG. There are both conventional and Shariah options available. To explore the companies in which both Conventional and Shariah ESG mandates invest, you can refer to the provided link.

3. PMART/PMA Blue Chip and Opportunity

Our Blue-Chip portfolios primarily allocate our investments towards companies with large market capitalisations, while the Opportunity portfolios predominantly invest in companies with smaller market capitalisations. We also offer both conventional and Shariah-compliant options to cater to the needs of all investors.

Please click on the link to learn more or email us at cse.my@phillipcapital.com.my if you require any further information.

Disclaimer

The information contained herein does not constitute an offer, invitation, or solicitation to invest in any product or service offered by Phillip Capital Management Sdn Bhd (“PCM”). No part of this document may be reproduced or circulated without prior written consent from PCM. This is not a unit trust or collective investment scheme and is not an obligation of, deposit in, or guaranteed by PCM. All investments carry risks, including the potential loss of principal.

Performance figures presented may reflect model portfolios and may differ from actual client accounts’ performance. Variations in individual clients’ portfolios against model portfolios and between one client’s portfolio to another can arise due to multiple factors, including (but not limited to) higher relative brokerage costs for smaller portfolios, timing of capital injections or withdrawals, timing of purchases and sales, and mandate change (e.g., Shariah vs. conventional). These differences may impact overall performance.

Past performance is not necessarily indicative of future returns. The value of investments may rise or fall, and returns are not guaranteed. PCM has not considered your investment objectives, financial situation, or particular needs. You are advised to consult a licensed financial adviser before making any investment decisions.

While all reasonable care has been taken to ensure the accuracy and completeness of the information contained herein, no representation or warranty is made, and no liability is accepted for any loss arising directly or indirectly from reliance on this material. This publication has not been reviewed by the Securities Commission Malaysia.

{kind=link}