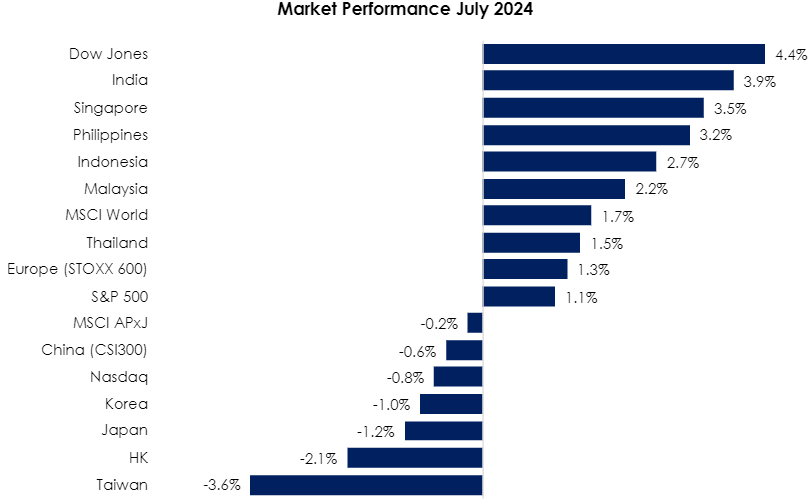

The MSCI Asia Pacific Ex-Japan Index (-0.2%) remained flat in July, dragged by weak performance in key markets while the MSCI World Index (+1.7%) raced ahead. India (+3.9%) advanced further, continuing its post-election rally and bolstered by investor confidence as 70% of urban Indians are positive on the national trajectory according to a survey by Ipsos. Singapore (+3.5%) came in at a strong second as banking and telco stocks registered strong single-digit gains during the month. Philippines (+3.2%) on the other hand experienced a much-needed reversal, breaking a four-month streak of consecutive losses as property sector stocks posted double-digit gains. Taiwan (-3.6%) cooled off in July after a spectacular 8.8% rally in June, amidst reports that the United States was considering tighter curbs on exports of advanced chips to China. Hong Kong (-2.1%) slid further down as investors remained skeptical on a market revival following China Third Plenum in mid-July. Japan (-1.2%) pulled back slightly as rate expectations in the US fuelled a tactical rotation into US growth stocks and small cap equities (see Exhibit 1).

Exhibit 1: Market Performance July 2024

Source: Bloomberg, PCM, 31 July 2024

The political landscape has shifted dramatically as Joe Biden’s withdrawal has led to a surge in support for Vice President Kamala Harris. A recent poll (31 July) by The Economist showed Donald Trump leading Harris only by one percentage point. Key upcoming dates include the Democratic National Convention on 19 August, the second presidential debate on 10 September, and Election Day on 5 November. Back in China, the Third Plenum Meeting ended without delivering the significant measures some had hoped for. Other significant events during the month included China People’s Bank of China (PBoC) cutting its 1-year and 5-year Loan Prime Rates (LPRs) by 10bps to record lows of 3.35% and 3.85% respectively, and the US Fed maintaining the FFR at 5.25%-5.50%.

Back home, FBMKLCI gained 2.2% MoM in July and closed at 1,625.57. Similarly, the Small Cap Index posted a positive return of 3.6%, while the Mid 70 Index gained 0.6%. Sector-wise, the top performers were Construction, Property, and Finance, with gains of 14.4%, 4.9%, and 4.1% MoM, respectively. Laggards were Healthcare, Technology, and Industrial, declining by -3.4%, -2.3%, and -2.0% MoM, respectively. In terms of fund flow, foreign investors turned net buyers in July, with the net buy flows of RM1.3bn substantially higher than the net sell flows of RM61m in June.

Strategy for the month

We think upcoming political election in the US will be the key event that may introduce greater policy uncertainties, which could have implications for sector positioning and security selection. Our analysis indicates that the investment case for US remains robust, bolstered by the corporates’ resilient earnings quality. Additionally, there is potential for a mean reversion trade given the deeply discounted valuations observed in the Chinese market. India has been one of the best-performing markets globally in local currency terms and has kept pace with US markets in dollar terms in recent decades.

A US recession will impact on the global economy which will means lower demand for oil and other commodities as well as manufacturing goods worldwide. US companies will also be faced with slower domestic economy and hence impact on corporate earnings. Based on past experience, market will be weak in the immediate terms but will recover when investors see the benefit of rate cut by the Fed which is initially scheduled for September. With the collapse of the US stock market as well as the plunge of Japanese stock market, the Fed is likely to accelerate the rate cut by 0.5% instead of 0.25% in September.

Back home, KLCI gained 11.8% over 7M24, driven by economic restructuring and fiscal reforms, record FDI/DDI, and strong corporate earnings momentum with upgrade by JP Morgan and on anticipation of cut in Fed rates in September. With the sudden fear of recession (probability of US recession in 2025 raised from 5% to 25-50%) due to much lower non-farm payroll that caused the collapse of US markets especially among the tech stocks. or even earlier. As our funds are mostly heavily invested, we may have to do switching strategy by selling stocks that have fallen less and buy more on stocks that have fallen more substantially. For investment where we intend to go for longer term, we will need to raise the portfolio beta but cautiously.

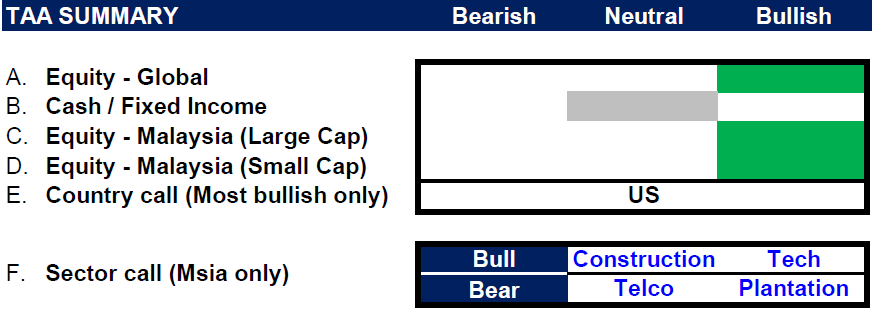

All in, we remain cautiously optimistic about the market, viewing the sharp correction as a potential buying opportunity for those who previously considered it too expensive. We prefer Hong Kong/China due to compelling valuations, and the U.S. market for its resilient earnings quality. In Malaysia, we continue to like large-cap stocks and remain bullish on selected small-cap stocks. Sector-wise, we favour the Construction sector, supported by project rollouts and data centre investments. Additionally, we favour the Technology sector, seeing indications of the semi down-cycle stabilising, along with companies poised to benefit from the current AI excitement. Conversely, we continue to hold our underweight stance in Telco and Plantation sectors (see Exhibit 2).

Exhibit 2: PCM’s monthly strategy snapshot

Source: PCM, 31 July 2024

Phillip Capital Malaysia and our offerings

We reaffirm our belief that there are still opportunities in the market, and we maintain a discerning approach in choosing high-quality stocks for our portfolio. However, it is crucial to exercise caution and carefully select investment options to ensure the best risk-adjusted returns. By taking a vigilant and discerning approach, investors can potentially reap the benefits of the current market opportunities while minimising risks.

A noteworthy avenue for investors seeking diversification in their portfolio is through PhillipCapital Malaysia. PhillipCapital Malaysia offers multiple private mandate services managed by professional fund managers. By leveraging PhillipCapital Malaysia’s private mandate services, investors can enhance their resiliency, optimise portfolio performance, and navigate the complexities of the market with confidence.

We also offer both conventional and Shariah-compliant options to cater to the needs of all investors. For Malaysia’s mandates, we like:

- PMART/PMA Dividend Enhanced and/or PMART/PMA Dividend Enhanced ESG

Our PMART Dividend Enhanced and PMA Dividend Enhanced is an income-driven portfolio focused on high dividend-yielding equities. We apply the Dog of the Dow approach, screen and select top market cap stocks to minimise risk and ensure consistent performance. The portfolio is an equal weighting portfolio which reduces concentration risk and provides similar exposure to all clients, both initially and after rebalancing. We offer both conventional and Shariah investment options to cater to the diverse needs of our investors. Click here to learn more. We recently also introduced PMART/PMA Dividend Enhanced ESG Mandate as we remain dedicated to investing in ESG stocks given their stronger valuation and profitability.

- PMART/PMA ESG

Phillip Capital Malaysia offers discretionary portfolio that invests in stocks with high ESG ratings from the F4GBM and F4GBMS Indices, namely PMART and PMA ESG. There are both conventional and Shariah options available. To explore the companies in which both Conventional and Shariah ESG mandates invest, you can refer to the provided link.

- PMART/PMA Blue Chip and Opportunity

Our Blue-Chip portfolios primarily allocate our investments towards companies with large market capitalisations, while the Opportunity portfolios predominantly invest in companies with smaller market capitalisations. We also offer both conventional and Shariah-compliant options to cater to the needs of all investors.

Please click on the link to learn more or email us at cse.my@phillipcapital.com.my if you require any further information.

Disclaimer:

The information contained herein does not constitute an offer, invitation or solicitation to invest in Phillip Capital Management Sdn Bhd (“PCM”). This article has been reviewed and endorsed by the Executive Director (ED) of PCM. This article has not been reviewed by The Securities Commission Malaysia (SC). No part of this document may be circulated or reproduced without prior permission of PCM. This is not a collective investment scheme / unit trust fund. Any investment product or service offered by PCM is not obligations of, deposits in or guaranteed by PCM. Past performance is not necessarily indicative of future returns. Investments are subject to investment risks, including the possible loss of the principal amount invested. Investors should note that the value of the investment may rise as well as decline. If investors are in any doubt about any feature or nature of the investment, they should consult PCM to obtain further information including on the fees and charges involved before investing or seek other professional advice for their specific investment needs or financial situations. Whilst we have taken all reasonable care to ensure that the information contained in this publication is accurate, it does not guarantee the accuracy or completeness of this publication. Any information, opinion and views contained herein are subject to change without notice. We have not given any consideration to and have not made any investigation on your investment objectives, financial situation or your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any persons acting on such information and advice.

{kind=link}