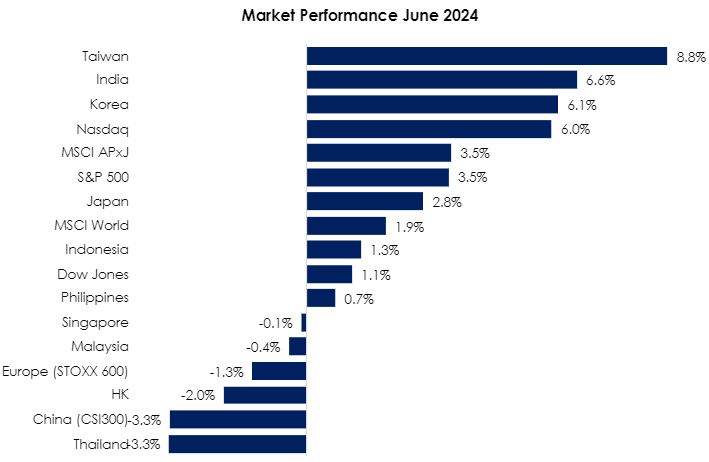

The MSCI Asia Pacific Ex-Japan Index (+3.5%) staged a comeback and significantly outperformed the MSCI World Index (+1.9%) in June on account of exceptional performance from Asia Pacific regional winners. Taiwan (+8.8%) continued its hot streak, as semiconductor tech names such as TSMC and Hon Hai surged strong double-digits on the back of the AI boom. India (+6.6%) came in at a strong second, bolstered by political tailwinds as a result of Prime Minister Narendra Modi’s election win and commitment from partners to form a coalition government. South Korea (+6.1%) came in at a close 3rd, bucking the trend of 2 consecutive losing months prior as memory players surged. Thailand (-3.3%) plummeted further, being the worst performing region YTD amid political uncertainties, with several key court cases on the horizon. China (-3.3%) and HK (-2.0%) also lagged the region as a slew of new tariffs by the US threaten to put even more pressure on China overcapacity narrative (see Exhibit 1).

Exhibit 1: Market Performance June 2024

Source: Bloomberg, PCM, 30 June 2024

Geopolitics has grown more complex as the US raised tariffs on Chinese imports, including EVs, semiconductors, and medical products in May, followed by the EU imposing higher tariffs on Chinese EVs in June. Subsequently, it was reported that Chinese domestic industries plan to request an anti-subsidy investigation into certain dairy products from the EU. While these developments are generally unfavourable, Malaysia could potentially benefit from trade diversion opportunities. Other significant events during the month included the ECB cutting rates by 25bps to 3.75% and the Fed maintaining the FFR at 5.25%-5.50%.

Back home, the FBMKLCI saw some profit-taking in June, losing -0.4% MoM and closing at 1,590.09. Conversely, the Small Cap Index posted a positive return of +3.6%, while the Mid 70 Index gained +2.1%. Sector-wise, the top performers were Construction, Technology, and Healthcare, with gains of +8.4%, +5.1%, and +2.3% MoM, respectively. Laggards were Consumer, Plantation, and REITs, declining by -2.3%, -1.3%, and -1.2% MoM, respectively. In terms of fund flow, foreign investors reversed their positions from net buying in May to a tiny net sell position in June, with net sell flows at RM61.4m, bringing the YTD outflows to RM823.2m.

In celebration of the 50th anniversary of Malaysia-China diplomatic relations, there is excitement surrounding the 11 MOUs valued at RM13.2 billion and mutual visa exemptions, which further bolsters business collaboration and tourism ties between the two countries. Additionally, investment themes expected to continue in 2H include the tech upcycle, accelerated private consumption, improving foreign tourist arrivals (and spending), and the initiation of a new investment cycle with announcements of new data centers and project awards. All in, building upon the robust market performance in 1H24, we anticipate further upside in 2H24. This outlook is supported by robust domestic factors such as earnings recovery, business policies, and political stability, along with external factors including China’s economic recovery and the upswing in the semiconductor industry.

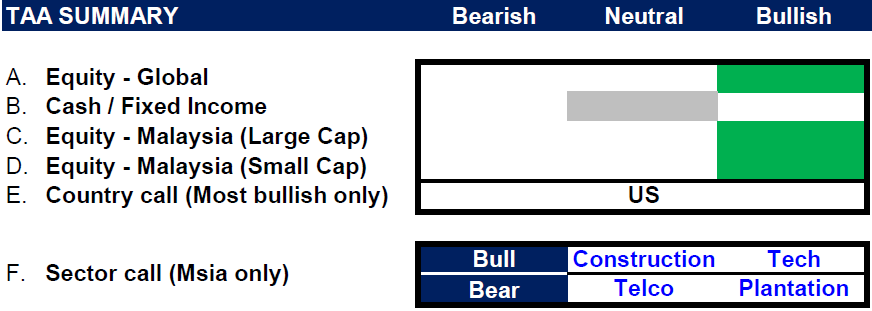

Strategy for the month

U.S. markets are currently testing new highs, as increased expectations of reacceleration of economic growth were supported by healthy job growth, strong corporate earnings and stubbornly high inflation number (still above 2.5% mark). Battle of the tech titans were almost a spectator scene; however we think upcoming political election in the US will be the key event that may introduce greater policy uncertainties, which could have implications for sector positioning and security selection. Our analysis indicates that the investment case for China remains robust, bolstered by governmental assurances to support the property sector. Additionally, there is potential for a mean reversion trade given the deeply discounted valuations observed in the Chinese market.

Investor focus is also keenly attuned to geopolitical developments, including the Hamas-Israeli conflict, Iran-Israel tensions, and the Russia-Ukraine situation, alongside global inflation trends, U.S. 10-year bond yields, global economic growth forecasts, and international interest rate trajectories. Our outlook on global equities remains cautiously optimistic, with a preference for Hong Kong/China due to compelling valuations, and the U.S. market for its resilient earnings quality.

In Malaysia, we continue to like large-cap stocks and remain bullish on selected small-cap stocks. Sector-wise, we favour the Construction sector, supported by project rollouts and data centre investments. Additionally, we favour the Technology sector, seeing indications of the semi down-cycle stabilising, along with companies poised to benefit from the current AI excitement. Conversely, we continue to hold our underweight stance in Telco and Plantation sectors (see Exhibit 2).

Exhibit 2: PCM’s monthly strategy snapshot

Source: PCM, 30 June 2024

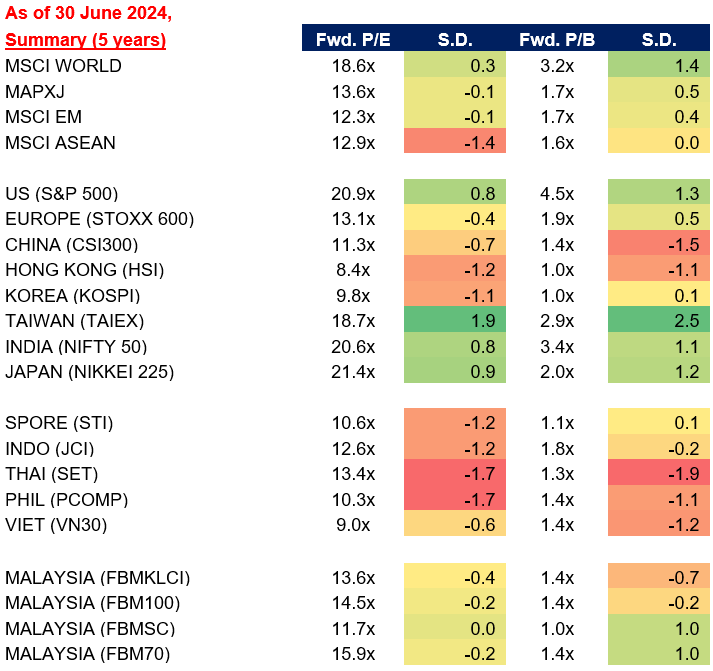

Exhibit 3: Selected Market Indices Valuations

Source: Bloomberg, PCM, 30 June 2024

Phillip Capital Malaysia and our offerings

We reaffirm our belief that there are still opportunities in the market, and we maintain a discerning approach in choosing high-quality stocks for our portfolio. However, it is crucial to exercise caution and carefully select investment options to ensure the best risk-adjusted returns. By taking a vigilant and discerning approach, investors can potentially reap the benefits of the current market opportunities while minimising risks.

A noteworthy avenue for investors seeking diversification in their portfolio is through PhillipCapital Malaysia. PhillipCapital Malaysia offers multiple private mandate services managed by professional fund managers. By leveraging PhillipCapital Malaysia’s private mandate services, investors can enhance their resiliency, optimise portfolio performance, and navigate the complexities of the market with confidence.

We also offer both conventional and Shariah-compliant options to cater to the needs of all investors. For Malaysia’s mandates, we like:

- PMART/PMA Dividend Enhanced and/or PMART/PMA Dividend Enhanced ESG

Our PMART Dividend Enhanced and PMA Dividend Enhanced is an income-driven portfolio focused on high dividend-yielding equities. We apply the Dog of the Dow approach, screen and select top market cap stocks to minimise risk and ensure consistent performance. The portfolio is an equal weighting portfolio which reduces concentration risk and provides similar exposure to all clients, both initially and after rebalancing. We offer both conventional and Shariah investment options to cater to the diverse needs of our investors. Click here to learn more. We recently also introduced PMART/PMA Dividend Enhanced ESG Mandate as we remain dedicated to investing in ESG stocks given their stronger valuation and profitability.

- PMART/PMA ESG

Phillip Capital Malaysia offers discretionary portfolio that invests in stocks with high ESG ratings from the F4GBM and F4GBMS Indices, namely PMART and PMA ESG. There are both conventional and Shariah options available. To explore the companies in which both Conventional and Shariah ESG mandates invest, you can refer to the provided link.

- PMART/PMA Blue Chip and Opportunity

Our Blue-Chip portfolios primarily allocate our investments towards companies with large market capitalisations, while the Opportunity portfolios predominantly invest in companies with smaller market capitalisations. We also offer both conventional and Shariah-compliant options to cater to the needs of all investors.

Please click on the link to learn more or email us at cse.my@phillipcapital.com.my if you require any further information.

Disclaimer:

The information contained herein does not constitute an offer, invitation or solicitation to invest in Phillip Capital Management Sdn Bhd (“PCM”). This article has been reviewed and endorsed by the Executive Director (ED) of PCM. This article has not been reviewed by The Securities Commission Malaysia (SC). No part of this document may be circulated or reproduced without prior permission of PCM. This is not a collective investment scheme / unit trust fund. Any investment product or service offered by PCM is not obligations of, deposits in or guaranteed by PCM. Past performance is not necessarily indicative of future returns. Investments are subject to investment risks, including the possible loss of the principal amount invested. Investors should note that the value of the investment may rise as well as decline. If investors are in any doubt about any feature or nature of the investment, they should consult PCM to obtain further information including on the fees and charges involved before investing or seek other professional advice for their specific investment needs or financial situations. Whilst we have taken all reasonable care to ensure that the information contained in this publication is accurate, it does not guarantee the accuracy or completeness of this publication. Any information, opinion and views contained herein are subject to change without notice. We have not given any consideration to and have not made any investigation on your investment objectives, financial situation or your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any persons acting on such information and advice.

{kind=link}