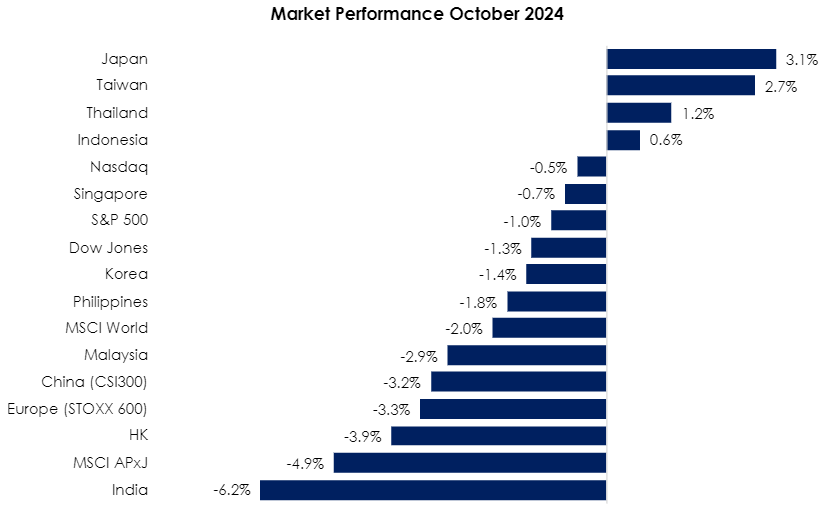

The MSCI Asia Pacific Ex-Japan Index (-4.9%) severely underperformed the MSCI World Index (-2.0%) in October, as China markets reeled back from their September rally, while a last-day pullback dragged down other regions. Japan (+3.1%) managed to close in the green for the month despite the Liberal Democratic Party’s (LDP) loss in the recent snap elections, which cost them their outright majority for the first time in 15 years. Taiwan’s (+2.7%) GDP grew faster than expected at 3.97% in 3Q24 driven by strong demand for smartphone and AI chips. Thailand (+1.2%) also managed to outperform most global peers thanks to upbeat growth guidance from government figures. India (-6.2%) was the month’s biggest loser as foreign funds flowed out of India on account of concerns over high valuations, presumably leading to reallocation into other markets. HK (-3.9%) and China (-3.2%) stumbled this month after overextending by approximately 20% gain in September, as investors cooled down and scrutinized the efficacy of the latest announced stimulus plans (see Exhibit 1).

Exhibit 1: Market Performance Oct 2024

Source: Bloomberg, PCM, 31 Oct 2024

In geopolitical developments, North Korea’s troop deployment to support Russia in Ukraine complicates regional tensions and poses challenges for China in balancing its alliances with both North Korea and Russia. Meanwhile, on the monetary policy front, the European Central Bank lowered its key interest rate by 0.25 percentage points to 3.25%, while China cut its one-year lending rate to 3.1% and its five-year rate to 3.6%.

Back home, the FBMKLCI fell 2.9% mom in October and closed at 1,601.88. Separately, Small Cap Index fell by 2.3% but the Mid 70 Index increased by 1.2%. Sector-wise, the top performers were Construction, REITs and Healthcare, with gains of 2.2%, 1.8% and 1.3% mom, respectively. Laggards were Utilities, Telco and Consumer, declining by -7.2%, -3.1%, and -2.5% mom, respectively. In terms of fund flow, foreign investors shifted to net sellers in October, recording net sell flows of RM1.8bn after three months of net buying. This reduced the cumulative foreign inflows to RM1.8bn for the first ten months of 2024.

Budget 2025 exemplifies the current administration’s earnest effort to improve the lives of the average Malaysian through shrewd reallocation of subsidy savings to finance wage hikes, larger cash handouts and not to mention an increased emphasis on transportation and social development projects, all initiatives that can be directly felt by the end consumer. We anticipate an uplift in the quality of life for B40 and M40 segments, with the Healthcare, Consumer Discretionary, Construction and Property sectors to be winners of 2025.

Strategy for the month

With Trump’s return for a second presidential term, investors should now shift their focus to how to strategically position themselves moving forward. We argue that market performance does not necessarily depend on the outcome of the US presidential election. Notably, “Change Election” has become the new norm in the US Since 2000, 10 out of 12 federal elections—including all of the last five—have led to a change in the party controlling the House, Senate, and/or the White House. This trend significantly exceeds the average from the 1960s to the 1990s, during which only one or two elections per decade resulted in a shift in party control. Despite this, the S&P 500 index has historically returned about 10% per year on average before adjusting for inflation, although the market tends to be more volatile during election years.

Trump’s 2024 trade policies are expected to mirror his “America First” approach, aiming to reduce the US trade deficit, protect American jobs, and challenge perceived unfair trade practices, particularly with China. Proposed measures include blanket import duties and a 60% tariff on Chinese goods, likely provoking retaliatory tariffs and raising import costs. This could lead to higher prices for US consumers and reduced demand, slowing global trade. In contrast, Malaysia has benefitted from the US-China trade war, with re-exports growing and foreign direct investment (FDI) surging, especially in sectors like electronics, semiconductors, and green technology. Malaysia’s strategic location also supports this trend.

In terms of market positioning, our preference in order is: US (strong earnings, positive economic data, proposed tax cuts) > Malaysia (policy) > Asia Pacific excluding Japan = Emerging Markets (benefiting from rate cuts) > China (valuation). Following the election, we have become more optimistic about the US market this month, as corporate earnings remain strong and economic data continues to show positive trends. Furthermore, Trump’s proposal to lower the corporate tax rate to 15% could improve earnings potential for US companies.

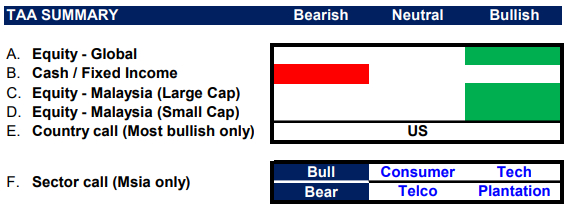

In Malaysia, we favour large-cap stocks and selected small-cap stocks. Sector-wise, we are optimistic about the Consumer sector, driven by pension hikes and EPF Account 3 withdrawals, which are expected to stimulate domestic consumption, and the Technology sector as semiconductor stabilization and AI opportunities emerge. Conversely, we continue to hold our underweight stance in Telco and Plantation sectors (see Exhibit 2).

Exhibit 2: PCM’s monthly strategy snapshot

Source: PCM, 31 October 2024

Phillip Capital Malaysia and our offerings

We reaffirm our belief that there are still opportunities in the market, and we maintain a discerning approach in choosing high-quality stocks for our portfolio. However, it is crucial to exercise caution and carefully select investment options to ensure the best risk-adjusted returns. By taking a vigilant and discerning approach, investors can potentially reap the benefits of the current market opportunities while minimising risks.

A noteworthy avenue for investors seeking diversification in their portfolio is through PhillipCapital Malaysia. PhillipCapital Malaysia offers multiple private mandate services managed by professional fund managers. By leveraging PhillipCapital Malaysia’s private mandate services, investors can enhance their resiliency, optimise portfolio performance, and navigate the complexities of the market with confidence.

We also offer both conventional and Shariah-compliant options to cater to the needs of all investors. For Malaysia’s mandates, we like:

- PMART/PMA Dividend Enhanced and/or PMART/PMA Dividend Enhanced ESG

Our PMART Dividend Enhanced and PMA Dividend Enhanced is an income-driven portfolio focused on high dividend-yielding equities. We apply the Dog of the Dow approach, screen and select top market cap stocks to minimise risk and ensure consistent performance. The portfolio is an equal weighting portfolio which reduces concentration risk and provides similar exposure to all clients, both initially and after rebalancing. We offer both conventional and Shariah investment options to cater to the diverse needs of our investors. Click here to learn more. We recently also introduced PMART/PMA Dividend Enhanced ESG Mandate as we remain dedicated to investing in ESG stocks given their stronger valuation and profitability.

- PMART/PMA ESG

Phillip Capital Malaysia offers discretionary portfolio that invests in stocks with high ESG ratings from the F4GBM and F4GBMS Indices, namely PMART and PMA ESG. There are both conventional and Shariah options available. To explore the companies in which both Conventional and Shariah ESG mandates invest, you can refer to the provided link.

- PMART/PMA Blue Chip and Opportunity

Our Blue-Chip portfolios primarily allocate our investments towards companies with large market capitalisations, while the Opportunity portfolios predominantly invest in companies with smaller market capitalisations. We also offer both conventional and Shariah-compliant options to cater to the needs of all investors.

TAA_Presentation_Deck_Nov-14.11.2024

Please click on the link to learn more or email us at cse.my@phillipcapital.com.my if you require any further information.

Disclaimer:

The information contained herein does not constitute an offer, invitation or solicitation to invest in Phillip Capital Management Sdn Bhd (“PCM”). This article has been reviewed and endorsed by the Executive Director (ED) of PCM. This article has not been reviewed by The Securities Commission Malaysia (SC). No part of this document may be circulated or reproduced without prior permission of PCM. This is not a collective investment scheme / unit trust fund. Any investment product or service offered by PCM is not obligations of, deposits in or guaranteed by PCM. Past performance is not necessarily indicative of future returns. Investments are subject to investment risks, including the possible loss of the principal amount invested. Investors should note that the value of the investment may rise as well as decline. If investors are in any doubt about any feature or nature of the investment, they should consult PCM to obtain further information including on the fees and charges involved before investing or seek other professional advice for their specific investment needs or financial situations. Whilst we have taken all reasonable care to ensure that the information contained in this publication is accurate, it does not guarantee the accuracy or completeness of this publication. Any information, opinion and views contained herein are subject to change without notice. We have not given any consideration to and have not made any investigation on your investment objectives, financial situation or your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any persons acting on such information and advice.

{kind=link}