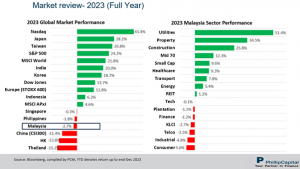

The MSCI Asia Pacific Ex-Japan Index (-4.8%) tumbled in January, underperforming the MSCI World Index (+1.1%) as weak performances in HK, China and South Korea dragged the former. Japan (+8.4%) had an incredible showing in January as renewed risk-on sentiment helped lift Japanese blue chips to record highs. Malaysia (+4.0%) had its best month in quite a while as strong foreign flows into blue chips breathed fresh excitement into markets pushing the index into levels unseen since Aug’22. Philippines (+3.0%) also had a strong showing as it overtakes Malaysia and Vietnam as the fastest growing economy in ASEAN. HK (-9.2%) and China (-6.3%) markets were devastated as waning investor confidence persist despite reports that China is planning a CNY 2tn rescue plan for the stock market. South Korea (-6.0%) also struggled in January despite a positive uptick in PMI levels and slowing inflation (see Exhibit 1).

Recent market volatility prompted significant efforts from China’s central bank, securities regulator, and state asset regulator. The securities regulator emphasises investor-centric capital markets, while the central bank implements a 50-basis points reserve ratio cut and other measures to support financial markets. The state asset regulator focuses on enhancing returns for investors, incorporating market value into the SOE appraisal system, encouraging share buybacks and increasing dividends. These measures aim to stabilise markets amid challenges such as Evergrande’s crisis and weak investor sentiment.

After an elongated period of rapid policy tightening, we view the Fed interest rate policy will begin normalising in 2024, signifying an inflection point by shifting from a ‘higher for longer’ view to a moderate pace before settling for a rate cutting cycle. The fall of interest rates expected in 2024 bode well for growth-oriented sectors and those that rely heavily on imports for production inputs. Separately, a weaker dollar eases the burden on deficit-laden governments and could potentially attract foreign inflows returning to emerging markets. On China, we expect more policy interventions and stimulus measures from the government and regulators to avert default in the property sector, including larger deficit spending by the government and potentially further interest rate cuts in 2024. The new growth areas such as Artificial Intelligence (AI), Electric Vehicles (EV), Renewables, Data Mining, Machine Learning, Cloud Computing and etc have the potential to expand further in China, transforming the economic structure over the longer term.

The domestic market kicked off the year on a positive note, posting a +4.0% gain MoM and closing at 1,512.98. During the month, the Small Cap Index trailed behind but still posted a positive return of +2.3%, while the Mid 70 Index gained +3.9%. Looking at the trading participants for the month, foreign investors remained net buyers, buying RM678.4m worth of shares. Local insti remained net sellers, selling RM662.9m worth of shares while retailers sold RM15.5m worth of shares. Foreign investors, in net, bought Utilities, Construction, and Financials sectors in January 2024, whereas Consumer, Industrial, and REITs sectors witnessed some outflows. Sector-wise, the top performers were Utilities, Energy, and Construction, with gains of +17.3%, +9.5%, and +9.4% MoM, respectively. Laggard was Technology, declining by -2.2% MoM (see Exhibit 1).

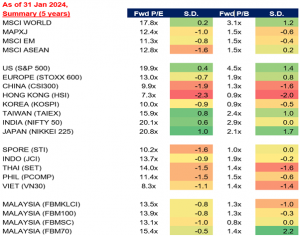

Looking ahead, we believe the local market is supported by continuous execution of the macro blueprints launched in 2023, robust domestic demand (amid normalising tourism and cash aids for B40 & M40) and a potential reversal in the strong US dollar trend. A US soft landing (or ideally a no-landing scenario) and gradual recovery in China could also offer some support to the local market. Furthermore, KLCI is supported by an undemanding valuation (13.5x forward P/E vs 10Y average 16.6x) accompanied by an all-time low foreign shareholding of 19.6% (as at Jan 2024). Other positive catalysts include a boost in Malaysian tourism due to China reopening, rising FDI momentum, and signs of the tech cycle bottoming out.

Exhibit 1: 2023 & 2024 Jan Market Performance

Strategy for the month

Several indications suggest the Fed may postpone an interest rate cut following recent hawkish remarks and sticky Jan’s inflation figures, compounded by the complexities of the Red Sea Shipping Crisis which could reignite inflation. While the labour market remains robust (low unemployment rate), consensus suggests potential weaknesses by year-end, reinforcing the argument for a rate cut. Nevertheless, our outlook on global equities remains cautiously optimistic, with a preference for the Hong Kong/China market due to appealing valuations and policy stimulus. Additionally, the US market is favoured for its strong earnings quality, presenting opportunities for investment during any potential pullback.

In Malaysia, we hold a positive view on large-cap stocks and selected small-cap stocks. Sector-wise, similar to the previous month, we favour the Construction sector, a beneficiary of Budget 2024, infrastructure project rollouts, and the National Energy Transition Roadmap. We have turned more positive on Technology as we see signs of down-cycle bottoming out. Conversely, we continue to hold our underweight stance in Telco and Plantation sectors. We have become less bullish on the Property sector due to its recent surge, while earnings may take some time to catch up.

Exhibit 2: Selected Market Indices Valuations

Source: Bloomberg, PCM, 31 Jan 2024

Phillip Capital Malaysia and our offerings

We reaffirm our belief that there are still opportunities in the market, and we maintain a discerning approach in choosing high-quality stocks for our portfolio. However, it is crucial to exercise caution and carefully select investment options to ensure the best risk-adjusted returns. By taking a vigilant and discerning approach, investors can potentially reap the benefits of the current market opportunities while minimising risks.

A noteworthy avenue for investors seeking diversification in their portfolio is through PhillipCapital Malaysia. PhillipCapital Malaysia offers multiple private mandate services managed by professional fund managers. By leveraging PhillipCapital Malaysia’s private mandate services, investors can enhance their resiliency, optimise portfolio performance, and navigate the complexities of the market with confidence.

We also offer both conventional and Shariah-compliant options to cater to the needs of all investors. For Malaysia’s mandates, we like:

- PMART/PMA Dividend Enhanced

Our PMART Dividend Enhanced and PMA Dividend Enhanced is an income-driven portfolio focused on high dividend-yielding equities. We apply the Dog of the Dow approach, screen and select top market cap stocks to minimise risk and ensure consistent performance. The portfolio is an equal weighting portfolio which reduces concentration risk and provides similar exposure to all clients, both initially and after rebalancing. We offer both conventional and Shariah investment options to cater to the diverse needs of our investors.

Click here to learn more

- PMART/PMA ESG

Phillip Capital Malaysia offers discretionary portfolio that invests in stocks with high ESG ratings from the F4GBM and F4GBMS Indices, namely PMART and PMA ESG. There are both conventional and Shariah options available. To explore the companies in which both Conventional and Shariah ESG mandates invest, you can refer to the provided link.

- PMART/PMA Blue Chip and Opportunity

Our Blue-Chip portfolios primarily allocate our investments towards companies with large market capitalisations, while the Opportunity portfolios predominantly invest in companies with smaller market capitalisations. We also offer both conventional and Shariah-compliant options to cater to the needs of all investors.

Please click on the link to learn more or email us at cse.my@phillipcapital.com.my if you require any further information.

Disclaimer:

The information contained herein does not constitute an offer, invitation or solicitation to invest in Phillip Capital Management Sdn Bhd (“PCM”). This article has been reviewed and endorsed by the Executive Director (ED) of PCM. This article has not been reviewed by The Securities Commission Malaysia (SC). No part of this document may be circulated or reproduced without prior permission of PCM. This is not a collective investment scheme / unit trust fund. Any investment product or service offered by PCM is not obligations of, deposits in or guaranteed by PCM. Past performance is not necessarily indicative of future returns. Investments are subject to investment risks, including the possible loss of the principal amount invested. Investors should note that the value of the investment may rise as well as decline. If investors are in any doubt about any feature or nature of the investment, they should consult PCM to obtain further information including on the fees and charges involved before investing or seek other professional advice for their specific investment needs or financial situations. Whilst we have taken all reasonable care to ensure that the information contained in this publication is accurate, it does not guarantee the accuracy or completeness of this publication. Any information, opinion and views contained herein are subject to change without notice. We have not given any consideration to and have not made any investigation on your investment objectives, financial situation or your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any persons acting on such information and advice.

{kind=link}