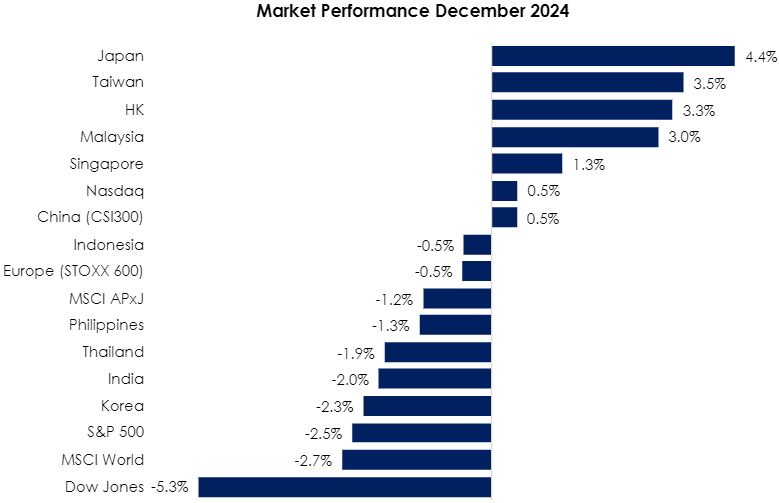

The MSCI Asia Pacific Ex-Japan Index (-1.2%) slightly outperformed the MSCI World Index (-2.7%) in December, albeit both were red on the month as regional markets pulled back after the Federal Reserve postulated a hawkish tone in December FOMC meeting and reduced rate cut forecasts for 2025 from 1.0% to 0.5%. Taiwan (+3.5%) led Asia Pacific thanks to TSMC gaining 10% on the month as its key customers, such as Nvidia and Apple, cited a better outlook on AI growth. Hong Kong (+3.3%) also rallied as the market retraced its gains after an extended decline since October. Malaysia (+3.0%) staged a surprise comeback in the last week of December, after a somewhat subdued 4th quarter where foreign funds left Malaysia to the tune of RM8bn in 4Q. On the flipside, South Korea (-2.3%) continued its decline and was Asia Pacific worst performer with a 9.6% loss in 2024, likely exacerbated by the seasonal cyclicality of its semiconductor-heavy index. India (-2.0%) declined moderately on weak economic data and persistently high inflation, coupled with heavy foreign fund outflows (~US$14bn in the first 2 months of 4Q). Lastly, Thailand (-1.9%) saw investors growing weary as central bankers flagged uncertainty on the impact of Trump 2.0 and looming US policy changes (see Exhibit 1).

Exhibit 1: Market Performance December 2024

Source: Bloomberg, PCM, 31 December 2024

On the monetary policy front, in December, the Fed lowered rates to a range of 4.25%-4.50%, but pointed to persistent inflation as the reason for anticipating fewer rate cuts next year. The European Central Bank (ECB) reduced its rate from 3.25% to 3.00%, while the Bank of England maintained its benchmark interest rate at 4.75%. Meanwhile, in Asia, the Bank of Japan (BOJ) kept interest rates steady at 0.25%. Finally, the People’s Bank of China held the medium-term lending facility rate at 2.0% and left the 1-year and 5-year loan prime rates unchanged at 3.1% and 3.6%, respectively.

Back home, the FBMKLCI gained 3.0% in December and closed at 1,642.33, bringing the 2024 return to 12.9%. Meanwhile, the Small Cap Index gained 3.9%, with a 2024 return of 9.9%, and the Mid 70 Index increased by 5.5% and a strong 28.9% in 2024. Sector-wise in December, the top performers were Technology, Healthcare, and Utilities, with gains of 11.1%, 10.5%, and 8.7%, respectively. Finance was the only laggard, declining by 0.1%. For 2024, the top performers were Construction, Utilities, and Property, with gains of 60.7%, 38.3%, and 31.5%, respectively. The laggards were Telco and Consumer, declining by 4.4% and 0.8%, respectively. In terms of fund flow, foreign investors continued to be net sellers for the third consecutive month in December, recording net sell flows of RM2.9bn, bringing cumulative foreign flows to a net outflow position of RM4.2bn for 2024.

Separately, in December, there was one listing on the Main Market (TMK Chemical Bhd), five listings on the ACE Market (Cropmate Bhd, Topvision Eye Specialist Bhd, Vanzo Holdings Bhd, Carlo Rino Group Bhd, and Winstar Capital Bhd), and two listings on the LEAP Market (Tp Tec Holding Bhd and Hydropipes Bhd). This contributed to a total of 55 listings in 2024 (Main: 11, ACE: 40, LEAP: 4), compared to 32 listings in 2023 (Main: 7, ACE: 24, LEAP: 1), reflecting strong growth across all IPO markets.

Equity Market Outlook & Investment Strategy

Malaysia

The Malaysian market has seen strong performance in 2024, driven by political stability, effective policy execution, and reflationary impacts from a stronger ringgit. Thematic plays, such as data centers, excitement around Johor, and tourism, have also contributed. Given the expected volatility with Trump taking office in January 2025, we will take a more strategic and cautious approach to stock and sector selection. We maintain strong investments in the technology and industrial sectors, as the US’s plans to raise tariffs on a wide range of Chinese imports, including semiconductors, batteries, solar cells and critical minerals, are expected to benefit Malaysia as multinational companies seek alternative investment destinations. Furthermore, the strengthening of USD is anticipated to positively impact sector earnings. Simultaneously, we are adopting a more agile investment approach, gradually increasing exposure to defensive sectors such as consumer goods and healthcare.

Regional

Global equities rebounded strongly in 2023 and 2024 following the 2022 correction due to the Ukraine-Russia war. With Trump back in office, his policies, including tax cuts, deregulation, and protectionism, are expected to benefit US equities. While China may face challenges from increased tariffs, the overall impact on the market will depend on how swiftly regulators adapt their policies to ensure economic stability. Additionally, with the US dollar expected to remain firm, fund flows are likely to favour the US, which may pressure regional currencies and impact market performance. Domestic-oriented economies such as India may fare better in this environment. Separately, Malaysia stands to gain from trade diversification, leveraging its strategic location, supply chain ecosystem, and skilled labour. While we remain cautiously optimistic about global equities, we believe that geopolitical tensions and protectionist trade policies could present risks to this outlook. As global markets grapple with heightened uncertainty, we emphasize the importance of diversification and a focus on quality amid volatility.

Fixed Income Outlook & Strategy

Malaysia

The BNM auction calendar for 2025 maintains 36 auctions but reduces the average issuance size to MYR4.56 billion, with the total MGS+GII supply forecasted at MYR164 billion (2024: MYR175 billion). The MGS/GII mix is evenly split, with 18 auctions each, and there is a notable shift towards more long-duration bonds, increasing 15- to 30-year issuances to MYR81 billion (49% of gross supply) while reducing short- to mid-tenor supply. The weighted average tenor is expected to lengthen to approximately 14 years. Despite the increase in long-duration supply, the market impact is anticipated to be manageable due to stable supply, limited net increases after private placements, and higher demand for longer durations. Minimal pressure is expected at the long end, though some steepening could occur if UST weakness persists.

The prevailing OPR level remains accommodative and conducive to sustaining economic growth. However, with inflation projected to increase in 2025, the likelihood of an OPR cut appears remote. Such a move would require a confluence of factors, including a sharp economic shock, a notable deterioration in the labour market, and sustained or intensified disinflationary trends.

Regional

As widely expected, the FOMC reduced its target range for the federal funds rate by 25 bps to the 4.25%-4.50% range at its December policy meeting. The FOMC has now cut its target range by 100 bps from its peak of 5.25%-5.50%, through moves of 50 bps in September, 25 bps in November, and 25 bps in December. Although the Committee eased policy in its final meeting of 2024, the market characterized the decision as a “hawkish” rate cut.

The annual inflation rate in the US rose for the second consecutive month to 2.7% in November 2024, up from 2.6% in October, in line with expectations. The rise is partly influenced by low base effects from last year. Energy costs declined less (-3.2% vs -4.9% in October), mainly due to gasoline and fuel oil, while natural gas prices rose by 1.8%, compared to 2%. Additionally, inflation accelerated for food (2.4% vs 2.1%) and prices for new vehicles fell much less (-0.7% vs -1.3%). On the other hand, inflation slowed for shelter (4.7% vs 4.9%) and transportation (7.1% vs 8.2%), and prices continued to decline for used cars and trucks (-3.4%, the same as in October).

The BoJ kept its benchmark rate at around 0.25%, in line with Bloomberg consensus expectations. Officials see no rush to delay a rate hike given the limited likelihood of significant upside inflation risks.

Strategy for the month

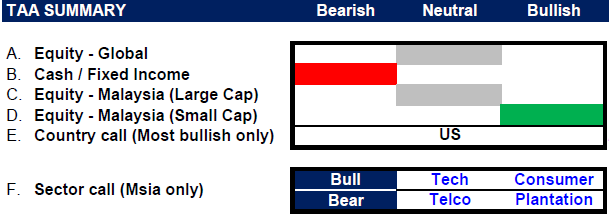

We turned neutral on global equities as geopolitical risks and rising inflation concerns continue to influence market sentiment. However, with the recent ceasefire between Israel and Hamas, the outlook is somewhat more positive, offering a glimmer of stability. In terms of market positioning, we are slightly more positive on the US, but not significantly so compared to Malaysia. We believe the strength of the dollar could weigh on Malaysia, potentially leading to foreign outflows. That said, we view the recent correction as a good buying opportunity for long-term investors, as US equities are poised for moderate growth this year, driven by tax cuts, deregulation, and strong corporate earnings, as well as continued innovation in AI that could boost margins.

In Malaysia, we maintain a neutral stance on large-cap stocks while continuing to favour select small-cap stocks. Sector-wise, we are positive on the Technology sector, with semiconductor stabilization and emerging AI opportunities. We are also optimistic about the Consumer sector, supported by civil servant salary hikes and EPF Account 3 withdrawals, which are expected to boost domestic consumption. However, we remain underweight on the Telco and Plantation sectors.

We became less optimistic about Asia Pacific ex-Japan after Trump’s win due to concerns that his trade policies, particularly the “America First” stance, would disrupt trade flows and economic relations in the region. Separately, the potential tariff hikes under the new Trump administration could negatively impact China‘s economy in 2025, though valuations have priced in many risks, and investor positioning in Chinese equities remains light. The net impact ultimately depends on China’s policy response.

Exhibit 2: PCM’s monthly strategy snapshot

Source: PCM, 31 December 2024

Phillip Capital Malaysia and our offerings

We reaffirm our belief that there are still opportunities in the market, and we maintain a discerning approach in choosing high-quality stocks for our portfolio. However, it is crucial to exercise caution and carefully select investment options to ensure the best risk-adjusted returns. By taking a vigilant and discerning approach, investors can potentially reap the benefits of the current market opportunities while minimising risks.

A noteworthy avenue for investors seeking diversification in their portfolio is through PhillipCapital Malaysia. PhillipCapital Malaysia offers multiple private mandate services managed by professional fund managers. By leveraging PhillipCapital Malaysia’s private mandate services, investors can enhance their resiliency, optimise portfolio performance, and navigate the complexities of the market with confidence.

We also offer both conventional and Shariah-compliant options to cater to the needs of all investors. For Malaysia’s mandates, we like:

- PMART/PMA Dividend Enhanced and/or PMART/PMA Dividend Enhanced ESG

Our PMART Dividend Enhanced and PMA Dividend Enhanced is an income-driven portfolio focused on high dividend-yielding equities. We apply the Dog of the Dow approach, screen and select top market cap stocks to minimise risk and ensure consistent performance. The portfolio is an equal weighting portfolio which reduces concentration risk and provides similar exposure to all clients, both initially and after rebalancing. We offer both conventional and Shariah investment options to cater to the diverse needs of our investors. Click here to learn more. We recently also introduced PMART/PMA Dividend Enhanced ESG Mandate as we remain dedicated to investing in ESG stocks given their stronger valuation and profitability.

- PMART/PMA ESG

Phillip Capital Malaysia offers discretionary portfolio that invests in stocks with high ESG ratings from the F4GBM and F4GBMS Indices, namely PMART and PMA ESG. There are both conventional and Shariah options available. To explore the companies in which both Conventional and Shariah ESG mandates invest, you can refer to the provided link.

- PMART/PMA Blue Chip and Opportunity

Our Blue-Chip portfolios primarily allocate our investments towards companies with large market capitalisations, while the Opportunity portfolios predominantly invest in companies with smaller market capitalisations. We also offer both conventional and Shariah-compliant options to cater to the needs of all investors.

Please click on the link to learn more or email us at cse.my@phillipcapital.com.my if you require any further information.

Disclaimer:

The information contained herein does not constitute an offer, invitation or solicitation to invest in Phillip Capital Management Sdn Bhd (“PCM”). This article has been reviewed and endorsed by the Executive Director (ED) of PCM. This article has not been reviewed by The Securities Commission Malaysia (SC). No part of this document may be circulated or reproduced without prior permission of PCM. This is not a collective investment scheme / unit trust fund. Any investment product or service offered by PCM is not obligations of, deposits in or guaranteed by PCM. Past performance is not necessarily indicative of future returns. Investments are subject to investment risks, including the possible loss of the principal amount invested. Investors should note that the value of the investment may rise as well as decline. If investors are in any doubt about any feature or nature of the investment, they should consult PCM to obtain further information including on the fees and charges involved before investing or seek other professional advice for their specific investment needs or financial situations. Whilst we have taken all reasonable care to ensure that the information contained in this publication is accurate, it does not guarantee the accuracy or completeness of this publication. Any information, opinion and views contained herein are subject to change without notice. We have not given any consideration to and have not made any investigation on your investment objectives, financial situation or your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any persons acting on such information and advice.

{kind=link}