Since the start of the year, the Malaysian market has been weak, primarily due to new US regulations on AI technology and China’s launch of DeepSeek. These developments sparked concerns over global AI capital expenditures, with domestic data center-related stocks facing potential earnings downsides. Additionally, the shift in Fed rate expectations, influenced by Trump’s tariff stance, added further pressure. An interesting observation is that, despite the overall market decline, the FTSE4Good Bursa Malaysia Index (F4GBM) saw a smaller drop (-10.23%) compared to the FBM Emas Index (-11.06%) as of 12 March 2025. To clarify, the FBM Emas Index includes the constituents of both the FBM Top 100 Index (which features large and mid-cap stocks) and the FBM Small Cap Index. On the other hand, the F4GBM Index consists of stocks from the FBM Emas with high ESG ratings (see Exhibit 1).

Exhibit 1: Performance Comparison of FBMKLCI, FBM Emas, and F4GBM

Source: Bloomberg, 12 March 2025

The smaller decline of the F4GBM Index compared to the FBM Emas Index can be attributed to several factors. Stocks in the F4GBM are selected for their high ESG (Environmental, Social, and Governance) ratings, which often correlate with strong corporate governance, sustainability practices, and better risk management. These factors may provide resilience during market downturns. Additionally, companies with high ESG scores are often seen as more future-proof, attracting long-term investors who prioritize sustainability. As a result, the F4GBM may have been less impacted by market volatility compared to broader indices like the FBM Emas.

Going forward, we see several factors supporting the potential for higher valuation multiples, including sustained strength in domestic investments (both DDI and FDI), ongoing fiscal consolidation (especially subsidy rationalization), and the strengthening of the Ringgit. While we expect elevated volatility in the short term due to uncertainties surrounding the Trump administration and policies, Malaysia, like other markets, experienced a broad decline. There are pockets of opportunity to invest in sustainable dividend-paying stocks and undervalued names that have been overly de-rated after the recent sell-off. Given the current macro environment, we remain positive on domestically driven sectors and direct beneficiaries of the NETR, such as Construction, Property, and Utilities. We are also optimistic about Financials, supported by growing confidence in Malaysia’s structural reforms and their sustainable dividend yields. Key risks include potential setbacks in Malaysia’s macroeconomic recovery and corporate earnings growth, driven by slower global economic growth and increased geopolitical risks.

Identify investment opportunities – Phillip Managed Account for Retirement (PMART) and Phillip Managed Account (PMA) ESG

In line with the nation’s goal towards sustainability, Phillip Capital Management has integrated ESG factors that we attest as material and relevant for a company’s financial performance and long-term sustainability into our investment decision-making process. These include but not limited to ESG ratings by established index, environmental considerations (climate change, natural resources preservation, pollution & waste), social considerations (health & safety, community engagement, employee relations) and governance considerations (board independence, transparency & disclosure, shareholder rights).

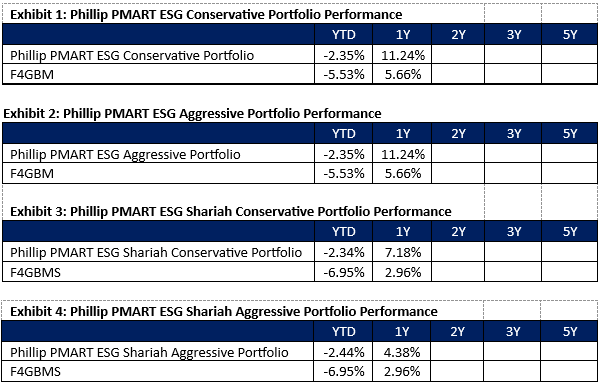

Separately, PCM offers PMART and PMA ESG, a discretionary portfolio that invests in stocks with high ESG ratings from the F4GBM and F4GBMS Indices. There are both conventional and Shariah options available. PMART and PMA ESG is suitable for investors who want to optimise the risk-adjusted return by constructing a diverse sustainable portfolio of ESG companies. Exhibits 1-4 show the performance for PMART ESG Conventional and Shariah.

Exhibit 2: Phillip PMART ESG Aggressive Portfolio Performance

Source: PCM, 31 Jan 2025, link

Comments on Performance:

The Malaysian market remained weak throughout the month, with mid and small-cap stocks lagging behind large-cap stocks. The results season was mixed, with sectors like oil & gas, technology, healthcare, rubber products, consumer, and auto underperforming, while plantations, transport, property, and basic materials exceeded expectations. Positive earnings revisions were seen in REITs, plantation, banking, and property. Valuation remains attractive with the KLCI trading at 13.8x P/E, 1 standard deviation below its 10-year mean. FBM Emas which comprises the big, medium and small cap companies in Malaysia now trades at 13.4x P/E, 1.3 standard deviation below its 10-year mean. We remain vigilant in our stock and sector selection against increasing macro risks from trade tensions and geopolitical uncertainties.

Please click on the link to learn more or email us at cse.my@phillipcapital.com.my if you require any further information.

Disclaimer:

The information contained herein does not constitute an offer, invitation or solicitation to invest in Phillip Capital Management Sdn Bhd (“PCM”). This article has been reviewed and endorsed by the Executive Director (ED) of PCM. This article has not been reviewed by The Securities Commission Malaysia (SC). No part of this document may be circulated or reproduced without prior permission of PCM. This is not a collective investment scheme / unit trust fund. Any investment product or service offered by PCM is not obligations of, deposits in or guaranteed by PCM. Past performance is not necessarily indicative of future returns. Investments are subject to investment risks, including the possible loss of the principal amount invested. Investors should note that the value of the investment may rise as well as decline. If investors are in any doubt about any feature or nature of the investment, they should consult PCM to obtain further information including on the fees and charges involved before investing or seek other professional advice for their specific investment needs or financial situations. Whilst we have taken all reasonable care to ensure that the information contained in this publication is accurate, it does not guarantee the accuracy or completeness of this publication. Any information, opinion and views contained herein are subject to change without notice. We have not given any consideration to and have not made any investigation on your investment objectives, financial situation or your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of any persons acting on such information and advice.

{kind=link}